Publié le 9 mars 2026 · 5 min read

By Thuy Lam, Advice-Only Certified Financial Planner at Objective Financial Partners in Markham, Ont.

As told to Ian Portsmouth

De notre commanditaire

Here’s the answer to this week’s reader question.

“How do I budget?”

—Jessica

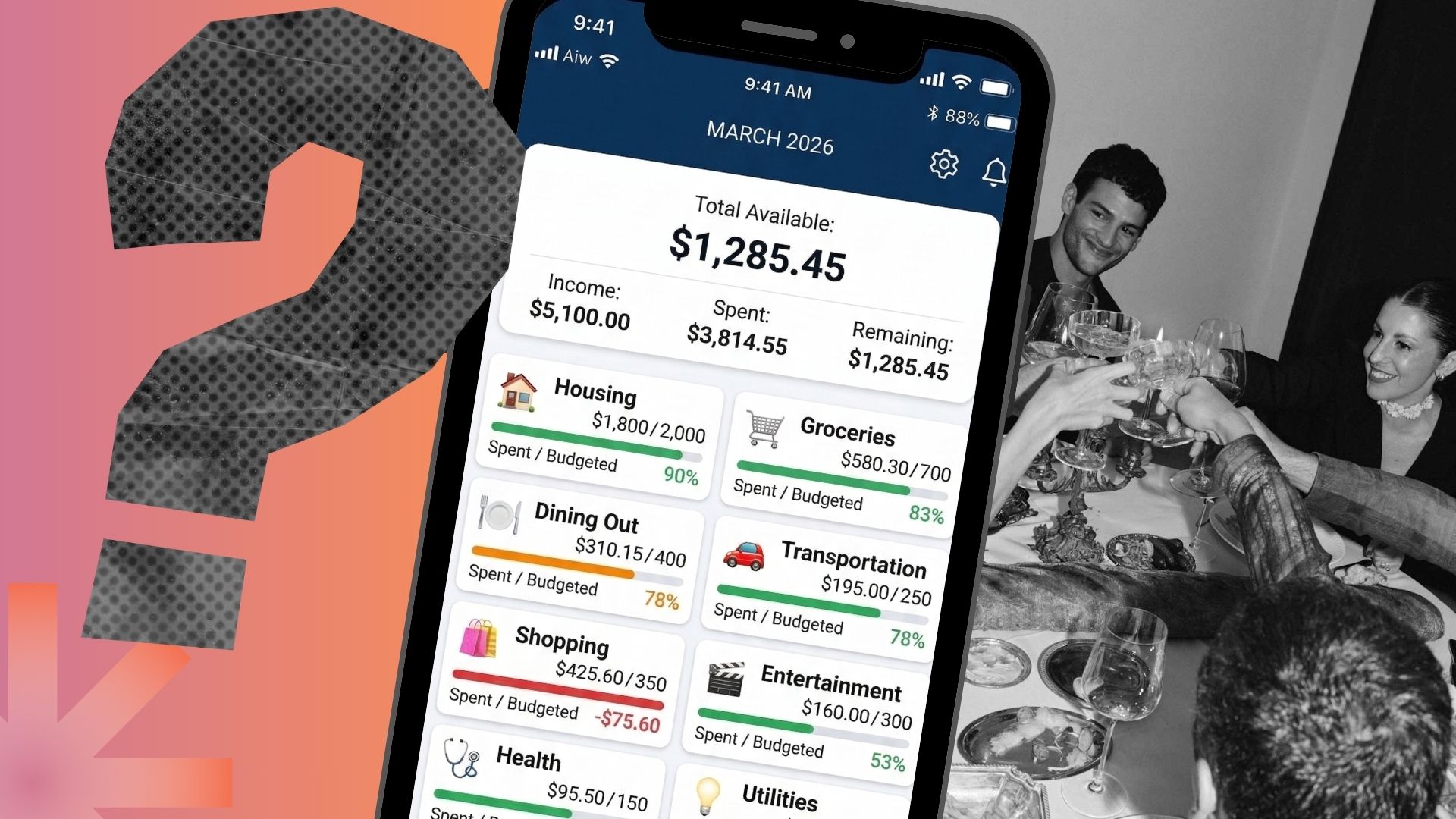

8 Steps to balancing a budget to reach your financial goals

Budgeting means different things to different people. For some, it means setting a strict spending limit. For others, it’s about figuring out where all their money goes each month. Personally, I think budgeting sounds restrictive and punitive. I prefer to think of it as creating and sticking to an “intentional spending plan”—a way to direct money toward what you value most.

Step 1: Understand your financial reality

Before creating your plan, you have to know what’s been happening with your money. That means gathering the full picture of your finances: what you own, what you owe, how much money comes in and how much goes out.

The most important piece is understanding your own spending. I strongly recommend reviewing a full year of expenses, because that captures predictable expenses, common discretionary purchases, emotional spending and other occasional or random expenses. If you look only at a shorter period, you’ll miss the variability.

Don’t worry about how much you spent or what you spent it on. This exercise is about gathering numbers, not judging yourself.

Step 2: Categorize your spending

Once you have the numbers, organizing your spending into several major buckets will help you see how your money flows. Typical categories include housing, transportation, communications (phone, internet), insurance, groceries, dining out, travel and entertainment, and services (accounting, home maintenance, hairstyling). You don’t need dozens of categories. The goal is clarity, not complexity.

When you finish this step, you can create a simple cash-flow statement that includes your monthly income, expenses and balance. How much of a surplus or deficit do you typically have at the end of a month? For many Canadians, this is the most eye-opening part of the process.

Step 3: Define your priorities

List your top three financial priorities for your current stage of life, such as building an emergency fund, paying off debt, saving for travel, investing for retirement or setting aside money for a child’s education.

For each priority, rank it, assign a dollar target and set a timeline to achieve it. For example, your top priority might be to pay off $2,400 in credit-card debt within a year. That means setting aside $200 a month.

These goals become the guidelines for your budget. Your spending decisions should support these goals.

Step 4: Compare your goals with your cash flow

This is where your intentions come face-to-face with reality. Once you know your spending patterns and your priorities, you can see whether your cash flow supports your goals. If you have extra money left each month, you can start directing it toward those priorities. If not, then you might need to adjust your spending, extend your timelines, change your priorities or find a way to increase your income.

Step 5: Create an intentional spending plan

Now, you’re designing the plan that will guide your spending going forward.

The idea isn’t to eliminate spending that brings you joy or benefits you in some other way. Buying takeout food regularly might be perfectly reasonable if it saves time or reduces your stress. The key question is whether your spending aligns with your priorities. If one of your financial goals matters more to you than a particular discretionary expense, then you need to shift the money accordingly.

Step 6: Build systems that make the plan easy

For many Canadians, it’s difficult to stick to a budget. Make it easier by aligning it with your normal habits or automating the process. For instance, you can set up automated debt payments and money transfers from your bank account. You can simplify expense tracking by isolating the payment method for a category you’re struggling to manage. For instance, using one credit card exclusively for takeout dining allows you to monitor your spending by checking your credit-card statement rather than collecting receipts and keeping a spreadsheet.

For shorter-term goals, I often recommend creating “electronic envelopes,” which are multiple savings accounts dedicated to specific goals. You can name them “vacation savings,” “emergency fund,” or whatever suits, then set up automatic transfers that will gradually build those balances.

When systems are in place, budgeting stops feeling like constant work.

Step 7: Review your progress

A budget isn’t something you set and forget. When the plan is new, it helps to check in monthly, especially on categories where spending can fluctuate. Over time, as your habits stabilize, those reviews can become less frequent.

At minimum, I recommend reviewing your budget annually to see whether your priorities have changed and how much progress you’ve made toward them. If you’ve achieved a goal, then redirect the money funding that goal toward a new objective.

Step 8: Celebrate small wins

This step is often overlooked, but it matters. Whenever you achieve a modest milestone or make meaningful progress toward one, celebrate that success. This little bit of positive reinforcement will build confidence in your financial habits and ability to reach your financial goals.

Budgeting is really about awareness

Budgeting isn’t about itemizing every receipt or counting every penny forever. Once you understand your spending patterns and build systems that support your priorities, budgeting becomes much simpler. Money should support the life you want to live.

A budget—or intentional spending plan—is simply the tool for making that happen.

Ian Portsmouth is an award-winning writer and editor specializing in business and personal finance. He is based in Toronto.

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.