Published on October 1, 2025 · 7 min read

What Is an Emergency Fund? A Guide To Your Financial Safety Net

Planning is an essential part of success. The more you thoroughly plan, the more you can be prepared when something happens, but what about the things you cannot plan for or don’t expect to happen? No matter how much you plan, you’ll never be 100% prepared for everything, as the future is unpredictable. That’s why having an emergency fund is important.

Your emergency fund helps you stay afloat in an unexpected event to prevent you from getting into financial trouble. A car accident, a flooded washroom, a sudden illness, or getting fired can happen to anyone and cause significant financial stress. The emergency fund is your plan to cover these unexpected costs.

But what exactly is an emergency fund, and why should you have one? This guide gives you all the insights on how to set up an emergency fund, why it’s important, tips on building your fund, and when to use it.

Setting up an emergency fund

Setting up an emergency fund may be one of your top priorities if you don't have one yet. You have many options when considering which account to use for your emergency savings. There are tax-sheltered accounts like tax-free savings accounts (TFSAs) and non-registered accounts like high-interest savings accounts (HISAs)

A high-interest savings account is a popular choice for keeping your emergency savings. Not only does it offer the accessibility of withdrawing your funds anytime, but you also enjoy low-risk growth from compound interest payments.

Setting aside money for your emergency savings is a part of a healthy financial routine. To ensure a sizable emergency fund, plan based on your budget and how much money you want to put into your emergency savings. Some experts advise putting aside enough money to cover at least three to six months of expenses.

Why emergency funds are important

Have you ever encountered an emergency or unexpected situation that caught you off guard? You don’t want to be caught with no backup plan when it comes to your finances and budget. Even the smallest financial setback can balloon into debt you don’t want to deal with.

The emergency fund acts as your backup plan in these situations. You withdraw money from your emergency savings to cover the unexpected costs since you set aside money for this purpose. You don’t have to take out loans, use credit cards, or withdraw from your savings or investments. It prevents you from getting into trouble that could cause long-lasting effects on your financial portfolio.

Tips to set up an emergency fund

A good strategy can make building an emergency fund easier to weather those rainy days. Here are some tips to consider so you can set yourself up for success and financial security when life throws a curveball at you.

Open a savings account

A savings account can be a great place to park any money you set aside for emergencies. There are two types of savings accounts– regular and high-interest savings accounts. The benefit of a high-interest savings account is that you earn a higher-than-average interest rate than regular ones.

When you have a high-interest savings account, you have a dedicated account to put your emergency funds. It helps organize your money allocation to various goals and prevents you from wanting to spend this money on non-emergencies.

You can access your money instantly whenever you want, which is good as emergencies happen unexpectedly, and you’ll need to withdraw funds quickly. Make regular deposits into the high-interest savings account to grow your emergency savings until you’re happy with the amount. You earn compound interest, which has an accelerated growth rate and can help you maximize your emergency savings risk-free.

Start by saving a realistic amount

Everyone starts their financial journey with zero funds and slowly grows their money to reach various goals. Start your emergency savings by setting a realistic amount that fits your financial situation. Consider your monthly income and expenses and determine how much you can afford to save. If your goal isn’t realistic, you may not be encouraged to set aside money regularly for your emergency savings, and it’ll be more difficult to make it into a habit.

You can write on a piece of paper what your target goal is when setting up your emergency fund. Some savings accounts have a feature that lets you set a budget or goal, and you can visually track your savings progress against that goal. For example, your goal can be to save $1,200 in your emergency fund in one year by saving $100 each month.

SMART goals stand for Specific, Measurable, Realistic, Attainable, Relevant, and Time-bound. Using SMART goals is a great way to ensure you have a defined action plan to achieve your goals within a specified timeframe. It eliminates guesswork and sets clear expectations for success. You can always review your progress against your SMART goals to keep you on track toward building an emergency fund.

Make it a habit

Incorporate savings into your daily habits to make it easier for you to reach your goal. There are a few ways you can start building your savings habit:

- Set reminders for yourself

- Set aside a specific amount of money every time you get paid

- Drop loose change into a jar

- Have a dedicated date where you put money into different savings goals

It takes a lot of consistency and discipline to successfully build a habit. There may be times when you want to spend extra dollars instead of putting them into your savings. Once you make it a habit to save money, it’ll become easier to grow your emergency savings.

Automate your savings

Automating your savings means you don’t have to think about saving money since the money automatically goes into your savings account. Choose a savings amount, date, and frequency to build your emergency fund. For example, you can automate your savings to deposit $100 into your savings account on the first of every month.

Eliminate an expense and save the amount

Eliminating expenses is a great way to save extra dollars. To determine the expenses you can cut, look at your budget and determine everything you spend money on. Keep any needs in your budget and cut down on some of the wants. A need is anything essential, such as rent and groceries. A want is something you enjoy having, like going to the movies or buying new clothes.

Once you identify your needs and wants, you can eliminate some of the wants you don’t want to spend money on anymore. For example, you may decide to save money by cooking at home instead of going to restaurants every week. Here are some other ways to eliminate expenses you may not need:

- Carpool or use public transportation instead of driving

- Make your coffee at home instead of buying at a coffee shop

- Bring a lunch to work or school instead of buying

- Use discount codes and coupons

- Shop when things go on sale

- Switch to generic items instead of brand names

Review your goals

Regularly review your goals against your financial situation and desired future state. Are your current goals still relevant? Can they help you get to where you want to be? Your family, personal, and work situation may change over time, so it’s important to update your goals to match your budget and lifestyle.

Important life events may include welcoming a child, buying a house, or starting a school program. When these events occur, review your goals and modify your budget accordingly so that your emergency savings remain a priority and a realistic goal.

Increase your emergency fund

Take advantage of opportunities to put more money into your emergency savings. Whether you cut expenses or increase your income, deposit as much as you realistically can into your emergency savings. You can also get creative by selling unwanted clothes or furniture. Any money left after paying your necessities and debts can potentially go towards your emergency savings.

You can start by raising your savings goal slowly. For example, once you reach $1,000 in your savings account, you can aim to save an additional $1,000. It makes it more achievable to increase your emergency fund at a comfortable pace.

Tips to help you use an emergency fund

It’s important to remember that your emergency fund should only be used in an emergency. Determine if you’re in an emergency or whether you can resolve the situation in another way. If you’re truly in an emergency, withdraw the necessary funds to help cover the expenses. Remember to set aside money in your emergency fund if you make withdrawals to ensure you have enough funds to cover a future emergency.

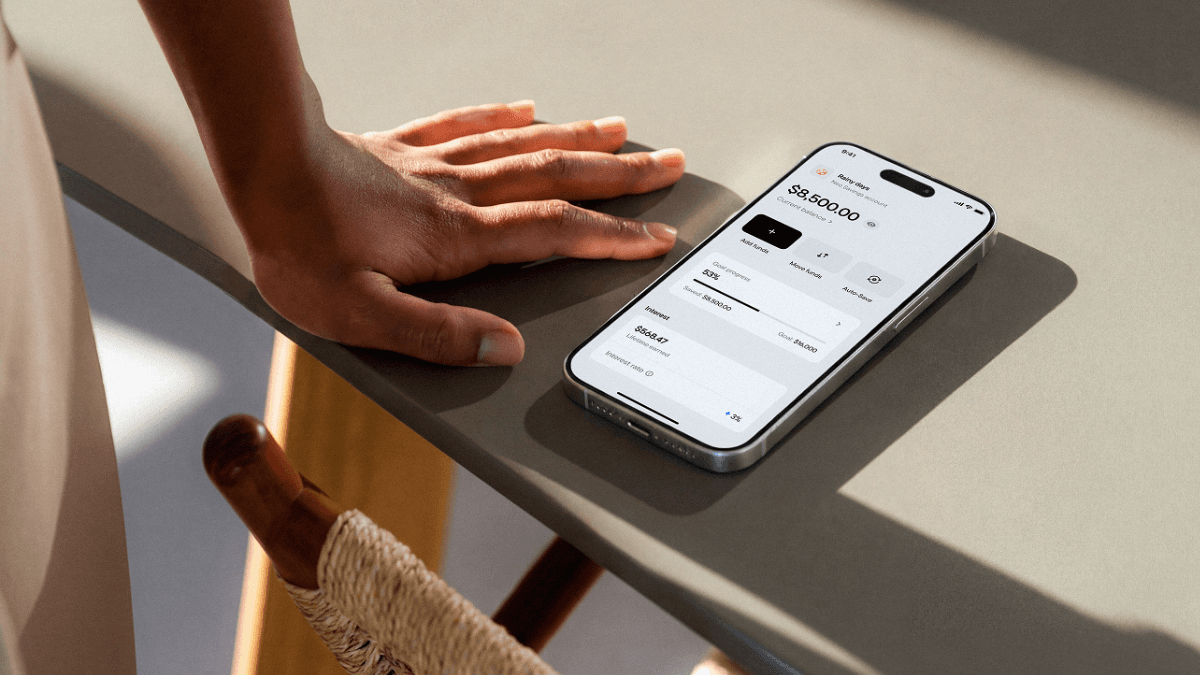

You should also find a reliable savings account to put your emergency savings. The Neo High-Interest Savings account is a great option. It offers a 4% interest rate¹ on your deposits, allowing your money to grow. You can access your money instantly and set goals to build good savings habits and increase your emergency fund over time.

Learn more about the Neo High-Interest Savings account and how it can help keep your emergency funds safe and ready to help you tackle unexpected expenses and get you back on track.

¹ Interest is calculated daily on the total closing balance and paid monthly. Rates are per annum and subject to change without notice.

Related Posts

View All

Here Are The Top 3 No-Fee Joint Bank Accounts in Canada

These are the best joint accounts in Canada that have no monthly fees, require no minimum balance and benefit from CDIC coverage.

The difference between chequing and savings accounts in Canada

A chequing account is for daily spending; a savings account earns interest. Here's how to use both.

The Best Youth Savings Accounts in Canada

The best youth bank account in Canada charge no monthly fees, pay a competitive interest rate, and give your child access to app-based banking so they can watch their balance grow.