Here’s the answer to this week’s reader question.

As told to Wing Sze Tang

“If I marry and have a lot of debt, does that debt also become a burden on my new spouse?”

—Stephen

In Canada, are debts shared in marriage?

The short answer: your debt doesn’t automatically become your partner’s responsibility when you get married. If you took out a student loan or had a credit card when you were single, and you signed that agreement on your own, that debt is just yours.

The long answer: yes, your debt can have an effect on your spouse.

On a financial level, for instance, if a lot of your income is going to debt payments, you’ll be less able to contribute to your household’s rent or mortgage, which may affect where you and your partner can live.

Having a lot of debt can affect your ability to borrow more money. You may have difficulty taking out a joint car loan or joint mortgage, because a lender will look at you and your partner’s overall debt load. And in this scenario, both credit scores will be taken into account.

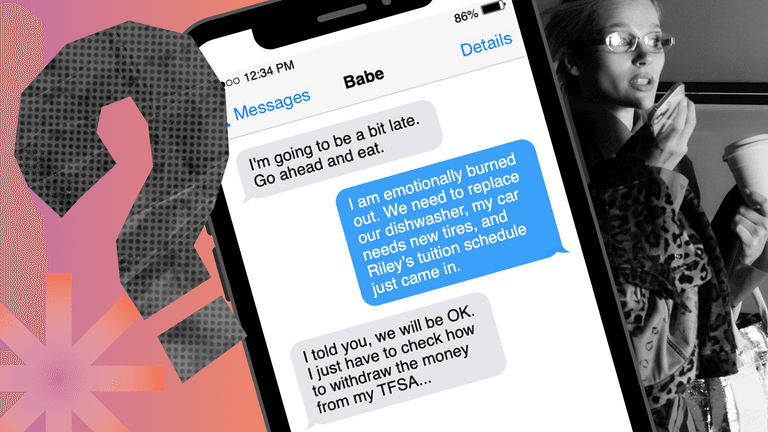

Beyond the financial impact, if you’re bringing debt into a marriage, that’s going to emotionally affect your relationship—especially if it’s news to your partner.

I don’t love the word “burden,” which is very emotionally charged. But entering a marriage while carrying debt can be very stressful. Even if your partner doesn’t legally have to pay off your debt, there’s still an impact on your relationship.

So, have that conversation as soon as possible, certainly before the wedding. If you don’t, it’s natural for your partner to feel like you weren’t being quite honest about your situation and yourself.

I’d recommend you be really clear about what led you to being in debt, and be upfront about the scope of the debt. Be ready with numbers. And then let your partner know your plan to pay it off.

There are some really great resources that can help you make a plan. For example, PowerPay is a debt reduction tool from Utah State University. I love it because it’s so easy to use and it’s free. It lets you input all your creditors and it generates a payment plan, month by month. And it gives you a date when you’ll be all paid off.

Finally, if you have shame or guilt about the way you deal with money, consider booking an appointment with a certified financial counsellor (CFC) to tackle any behavioural or emotional issues that led you into this situation. They can help you improve your financial well-being through better money management, behavioural counselling and financial literacy. And talking to a CFC is also a great way to show your partner, “I’m working on this.”

—Wendy Underwood

Founder, Lifeform Financial Coaching

Have a question for us? Send it to TheGet@neofinancial.com.

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.