Mis à jour le 24 juin 2026 · Publié le 25 mai 2026 · 4 min read

By Stephanie Debisschop, executive director of the Plan Institute

As told to John Loeppky.

Here is the answer to this week’s reader question.

I have a 22-year-old son. He is disabled and qualifies for the Disability Tax Credit (DTC). We didn’t start an RDSP before he turned 18, but can he still open one now and have the government match his contributions?

I am also disabled. If I could come up with money to open an RDSP, would I qualify for grants, bonds or the government’s matching contributions?

—Corrine

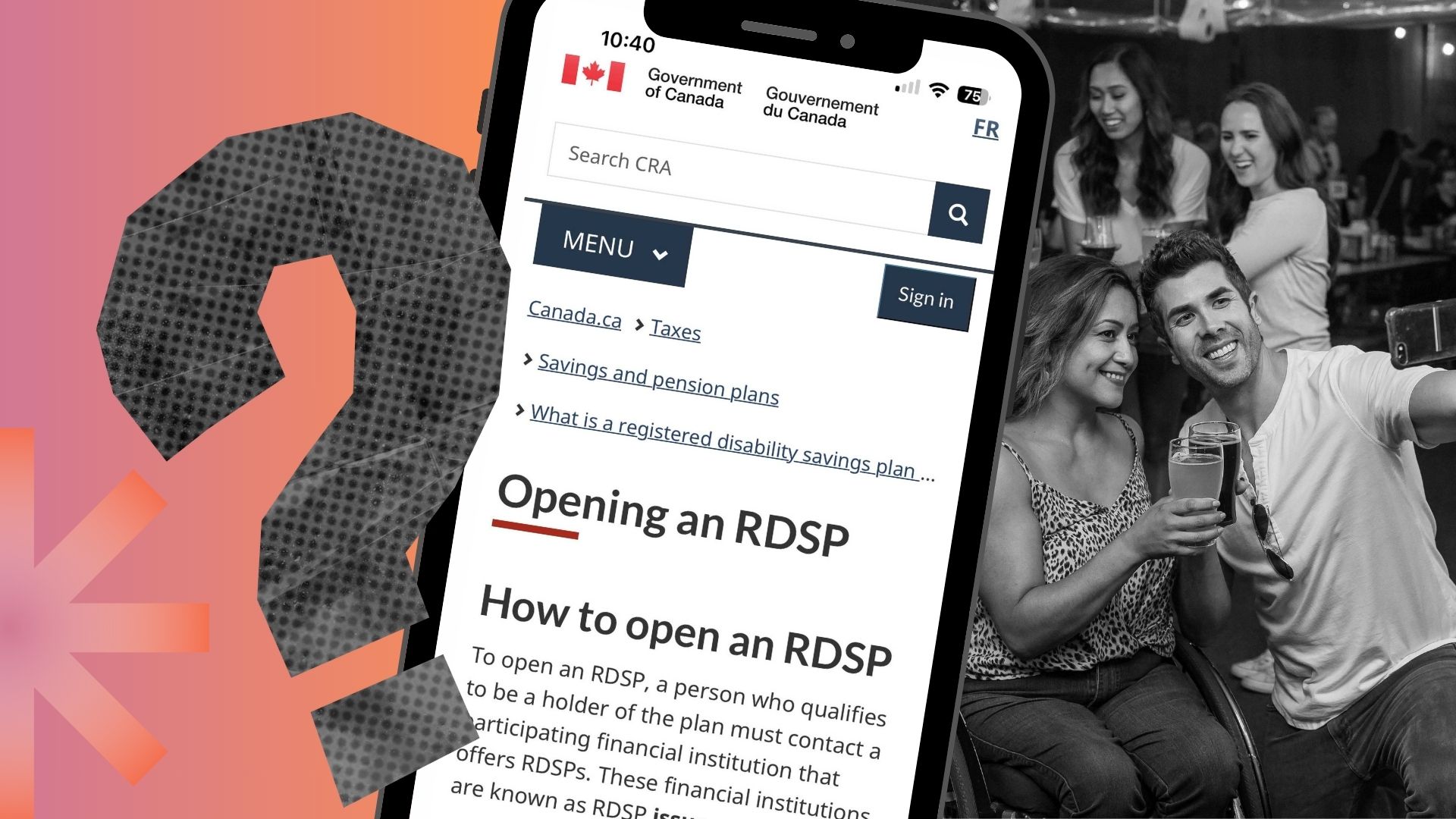

How late is too late to open an RDSP?

Yes, you can open a registered disability savings plan (RDSP) for your 22-year-old son. But opening one for yourself depends on a few things. But let’s get into RDSPs—how they work, and what you and your son may qualify for with them.

There really are three key elements to a registered disability savings plan.

- There’s anything that you or a loved one contributes into your RDSP.

- There are matching grants and bonds.

- Those matching amounts vary by income level; the higher your income, the lower the ratio used to calculate the matching amount.

The calculation of the matching amounts is based on income and how much you’ve contributed. You can project the future value of an RDSP with a calculator on the Plan Institute’s website.

There’s no fee whatsoever for the RDSP itself. If you don’t put any money in, you wouldn’t be able to receive matching grants from the federal government, but having the RDSP still entitles you to receive the bond of up to $1,000 a year for a maximum lifetime amount of $20,000.

That’s $1,000 a year for 20 years, as long as you fall within the program’s income threshold. We would always advocate to open an RDSP whenever possible. If you start early, any returns can be compounded into a really meaningful sum.

The reality, though, is that often an RDSP isn’t the priority for parents and guardians who have a child with a disability. They’re paying for all sorts of things in caring for and setting up the future for their child.

Forty-nine is the important age to remember for receiving retroactive grants and bonds. By the end of the calendar year in which you turn 49, you can open an RDSP and get retroactive grants for 10 years—if you would have qualified for them. You can set up an RDSP anytime until the end of the calendar year that you are 59, but you wouldn’t receive those matching grants and bonds.

If you have an insurance claim as a result of an injury that’s led to your disability, you can open up an RDSP and it shelters those funds from impacting your provincial or territorial benefits.

The RDSP is not a short-term or emergency vehicle. It’s meant to be more long-term. But, you can withdraw funds earlier if there’s a shortened life expectancy.

Our disability planning helpline, which offers free support to people from coast to coast to coast, often addresses questions about navigating the systems of benefits as a whole—whether it relates to the Canada Disability Benefit (CDB), the Disability Tax Credit (DTC), an RDSP, a provincial or territorial benefit, or something else that might be needed or available.

If the paperwork wasn’t so complex, there wouldn’t be a need for such deep support in navigating these systems. The underfunding and under-availability of free community-based supports in navigating these benefits creates an environment where predatory companies can flourish.

I think all of these questions are within a broad context of the systemic barriers that exist, creating an environment of legislated poverty. There is so much potential to alleviate these pain points that folks are experiencing every single day. There's so much possibility to streamline disability benefits in a way that would mean fewer barriers, fewer negative impacts, less cost, less stress and less re-traumatizing.

John Loeppky is a British-Canadian journalist currently living and working on Treaty 6 territory in Saskatoon. He is writer and host of History in 60, a television show focused on Canadian disability history that airs on Accessible Media Inc (AMI).

Read more from this issue of The Get:

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.