Published on October 1, 2025 · 8 min read

The perfect savings account amount: How much should I put in my savings every paycheque?

Budgeting can be hard. Besides saving money, you also have bills, investments, retirement funds, and daily expenses to think about. You have several financial obligations and a limited amount of money every paycheque.

If you’ve ever wondered how much money you should put in your savings every paycheque, you’re not alone. While there’s no right answer, there are some guidelines for finding the perfect number based on your unique financial situation.

Assessing your current financial situation

It's important to assess your current situation before making any financial decisions. It’s hard to allocate your money accurately if you don’t understand how much you can afford to save. The first step is to understand your cash flow versus your expenses.

Your cash flow is the money going in and out of your account, which includes any income streams and expenses. Understanding your cash flow can help you determine whether you have leftover funds to put into a savings account. List your incomes and expenses on a paper or spreadsheet, such as jobs, investment earnings, and fixed and variable expenses. Expenses include any fixed or variable expenses, such as monthly bills, groceries, gas, shopping sprees, and subscriptions.

Here are some questions you can ask yourself as you assess your current financial situation:

- How much do I earn every month?

- What are my expenses each month?

- How can I reduce my monthly expenses?

- Do I have a budget?

- Do I have good financial habits?

- What are my short-term and long-term goals?

Answering these questions can help give you a better perspective into your overall financial health to determine whether you have the means to save and reach your goals.

Determining what you’re saving for

Having goals is important as it gives you something to work towards and motivates you to stay on track. Your savings goals will likely change as you reach milestones and prioritize different things.

Whether you’re a student saving for tuition or looking to retire and travel the world, you should have an idea of what you’re trying to achieve (and how much you need to achieve it). You’ll then have a better understanding of how much money you need to save and help you stay on top of your progress.

Here are three common categories of savings goals many people have:

Emergency fund

An emergency fund is an amount of money set aside for emergencies. It’s a financial safety net for any unexpected expenses or mishaps that may occur. Even the smallest financial shock can set you back and snowball if you don't have an emergency fund.

While the future is unpredictable, and you can’t always predict what may happen, you can reduce risk and exposure through an emergency fund. Some common emergencies include medical bills, home repairs, car repairs, loss of income, and unexpected changes in living situations.

You can rely on your emergency savings for large or small unplanned expenses that aren't part of your financial routine. You should only use your emergency savings in a real emergency. You shouldn't use the funds as an extra cash reserve when your daily banking account runs out of money.

The amount of money you keep in your emergency savings depends on your situation. A rule of thumb is to have enough money to cover three to six months of your expenses.

Short-term savings goals

Short-term savings goals refer to anything you want to achieve within five years. Everyone’s short-term savings goals are different depending on the stage they’re in, their needs, and wants. Examples of short-term savings goals may include buying a house, going on a vacation, buying a car, or buying an expensive computer.

Having short-term savings goals ensures you have the financial means to buy the things that improve your quality of life right now. It also helps you build a strong foundation for achieving bigger long-term goals.

Long-term savings goals

Long-term savings goals take more than five years to achieve. These are typically the bigger items on your list. Examples include paying your mortgage, saving for a child’s college education, and funding your retirement.

Long-term savings goals are generally more expensive than short-term ones, so start planning for them early. If you set aside a little bit of money frequently, it adds up over the years, and you’ll be able to reach these goals.

Create a budget you feel comfortable with

A budget gives you a better understanding of your cash flow at all times and helps control your spending to stay within your means. You may have heard of the 50/30/20 rule before. However, there’s no specific rule to follow as your budget depends on your situation and goals.

If you want to save more money and have the means to set aside larger amounts in a savings tool, go for it. If you don’t have as much money to set aside, start by saving smaller amounts and slowly increase your savings in the future. Instead of worrying about which template to use to create your budget, it’s more essential to choose a strategy that works for you and stick with it in the long-term.

It’s also essential to review your budget periodically to ensure it still aligns with your financial situation or goals. Review your cash flow monthly and determine how much money you spent. If you went over budget, consider the reasons why you spent too much money. If you were under budget, determine whether you can readjust your budget to save more each month.

If you’re looking for inspiration to build better savings habits, consider these tips:

- Track your daily spending

- Spend less than you make

- Re-evaluate your wants and needs

- Look for deals

- Find people to keep you accountable

- Make an effort to spend less during specific periods

Identify how much money to put into savings with every paycheque

Based on your financial assessment, determine how much money you can afford to save each month. Look at how much income you earn in comparison to your monthly expenses, like bills and debts. Regardless of what you prioritize in your financial plan, make sure you have a plan to meet your various obligations.

If you’re just starting to save, you can build up your savings by setting aside a little bit of money with every paycheque, like 5-10 dollars. Create a goal, like saving $1,000 in one year. If you find $1,000 to be a challenging goal, lower the amount. The goal is to have an attainable and realistic number in mind to build good discipline and habits.

How much of your paycheque to save

With your pay statements and expenses, you most likely have a good idea of your monthly cash flow already. The amount you save from each paycheque largely depends on what makes you comfortable and your savings goals.

You can always lower the percentage you save with each paycheque if you feel overwhelmed or strapped for cash all the time. You can also increase the percentage if you have extra cash. The savings goal is simply a guideline to ensure a sizeable savings fund to meet your financial goals.

Look at the amount and frequency of your paycheques, such as monthly, bi-weekly, or twice a month. Determine how much of your paycheque goes towards expenses and how much you can allocate towards savings. For example, if you earn $2,500 per paycheque and spend $1,500 on expenses, you can save $1,000.

The amount you save from each paycheque can change as your income or expenses increase or decrease. Aim to save as much as it makes sense for your situation and future goals. If you have a lot of debt, tackle your debts first before putting money into your savings. If you have a higher income or don’t have a lot of expenses, you can aim to save more of your money.

Ensure you’re saving in the right account

Putting your savings into the right account is as important as saving money with every paycheque. There are tons of accounts available designed to support your various goals and ensure you optimize your financial situation.

If you’re looking for the best place to put your savings, look no further than a high-interest savings account. A high-interest savings account is a safe place to park your savings from each paycheque and earn interest based on your account balance. Not only do you earn a competitive interest rate compared to a traditional savings account, but it’s also a low-risk account to help you reach your goals quickly.

Many people use high-interest savings accounts for short-term savings goals and emergency funds since you earn interest and keep your deposits. A high-interest savings account offers many perks and features designed to help maximize your savings:

- High interest rate

- Low-risk savings

- Security

- Flexibility and accessibility to your funds at any time

- No fixed, monthly fees

- No minimum balances

Note that these benefits may not apply to all high-interest savings accounts as different financial providers set their own rules and restrictions. It’s important to find a high-interest savings account that aligns with what matters most to you.

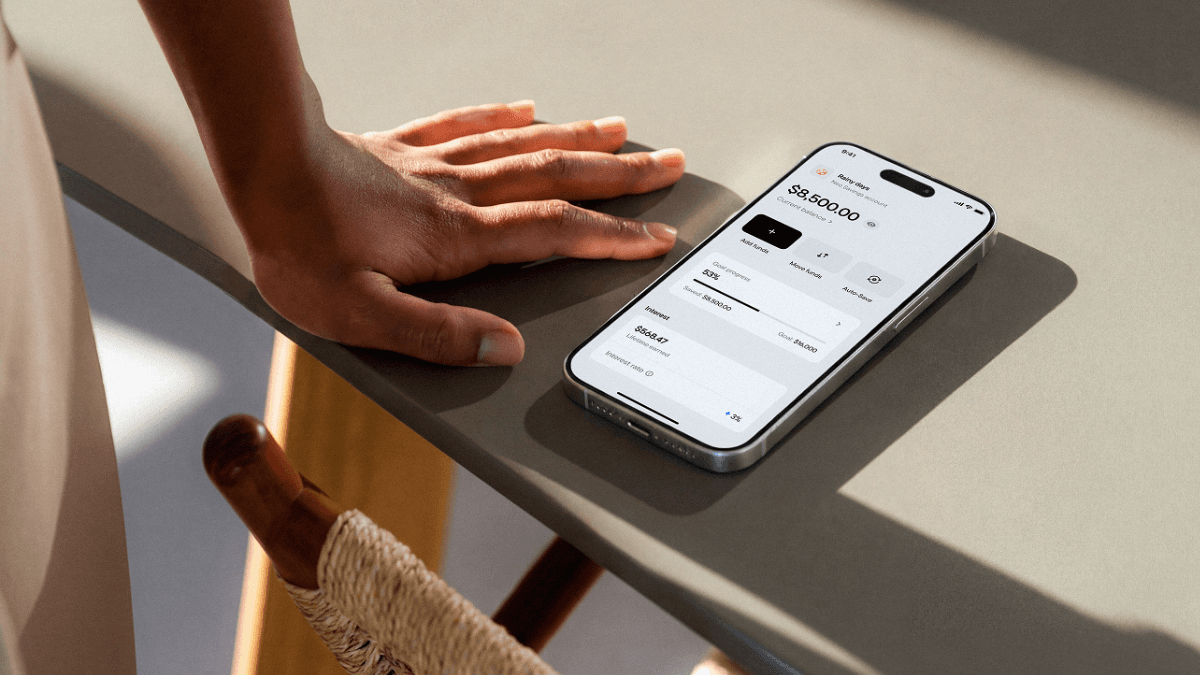

The Neo High-Interest Savings account is ideal if you want an account that matches all the benefits listed above. With 4% interest¹ on every dollar deposited, your money works hard to ensure you maximize your savings.

You can open multiple high-interest savings accounts and personalize them to save for different goals. Track your savings, habits, and progress all from the intuitive Neo app. The Neo app also makes it easy to set aside money for your savings with every paycheque with features like Auto-Save!

Learn more about the Neo High-Interest Savings account today and get started in a few minutes.

¹ Interest is calculated daily on the total closing balance and paid monthly. Rates are per annum and subject to change without notice.

Related Posts

View All

The difference between chequing and savings accounts in Canada

A chequing account is for daily spending; a savings account earns interest. Here's how to use both.

The best youth savings accounts in Canada

The best youth savings accounts in Canada charge no monthly fees, pay a competitive interest rate, and give your child access to app-based banking so they can watch their balance grow.

4 high-interest savings account (HISA) ETFs Canadians should know

Looking for a low-risk place to park cash inside a brokerage account? Consider these four HISA ETFs.