By Julien Brault, founder of MooseMoney.

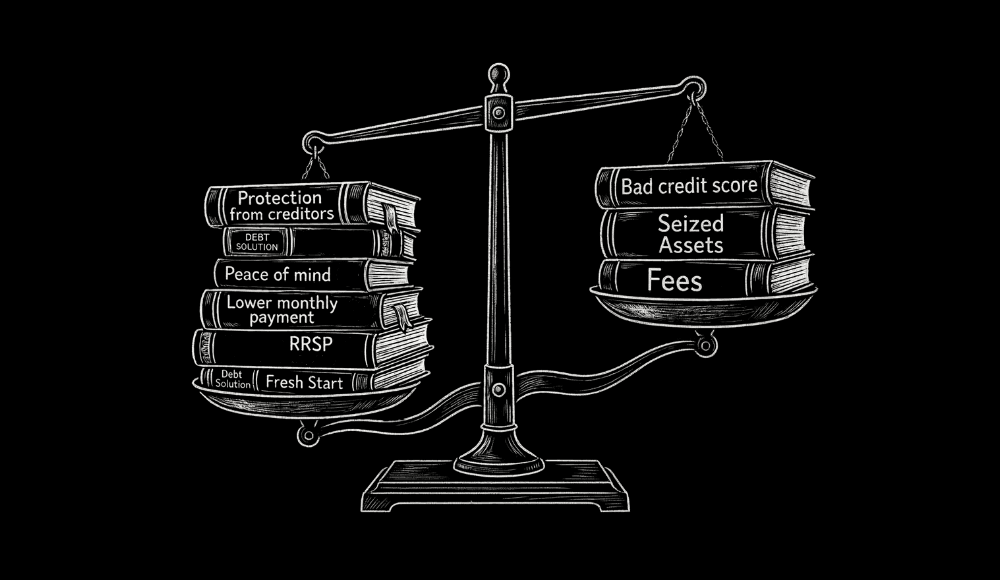

A consumer proposal stops collection calls, freezes interest on unsecured debts, and lets you repay a fraction of what you owe over up to five years. Those are the well-known benefits. What most Canadians do not anticipate are the secondary consequences that ripple through their life long after the paperwork is filed. Here are ten effects of a consumer proposal that often catch Canadians off guard:

1. Your credit score may not drop as far as you think

Many filers assume a consumer proposal will destroy a previously strong credit rating. In practice, most people who reach this stage already carry missed payments, maxed-out utilization, or collection accounts that have already dragged their score down. Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp, observes, "By the time the debtors come to us, their credit score is most often very low already or it's about to be very low because they can no longer pay their debts on time." A consumer proposal places an R7 rating on each included account, which is lower than the R9 assigned in bankruptcy. If your report already shows multiple R9 or collection entries, the net impact on your score can be smaller than expected.

2. You can apply for a secured credit while still in the proposal

There is a common misconception that your credit score is stuck in the mud until your consumer proposal is completely finished. In reality, nothing in the Bankruptcy and Insolvency Act prevents you from actively repairing your credit while your proposal is still running. The most effective way to do this is by applying for a secured credit card, such as the Secured Neo Mastercard. Because these cards are backed by your own refundable security deposit, lenders are happy to approve you. By using the card responsibly and paying your statement balance in full every month, you start generating a fresh, positive payment history on your credit report long before your proposal officially ends.

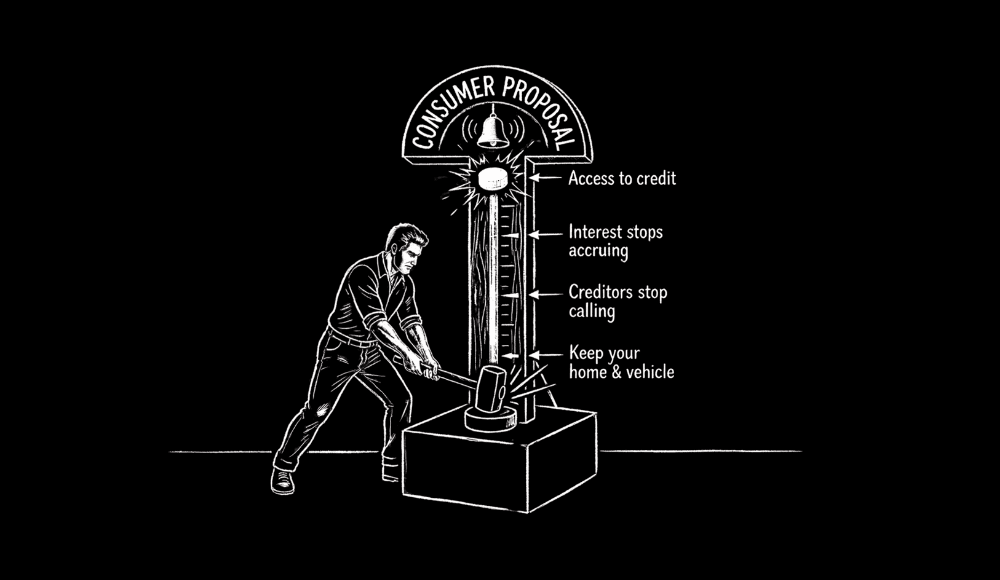

3. Creditors must stop all contact and legal action immediately

The automatic stay of proceedings takes effect the moment your Licensed Insolvency Trustee files the proposal with the Office of the Superintendent of Bankruptcy. Wage garnishments halt, collection agencies must stop calling, and any pending lawsuits related to your unsecured debts are stayed. Many filers describe this sudden silence as the single most unexpected relief of the entire process.

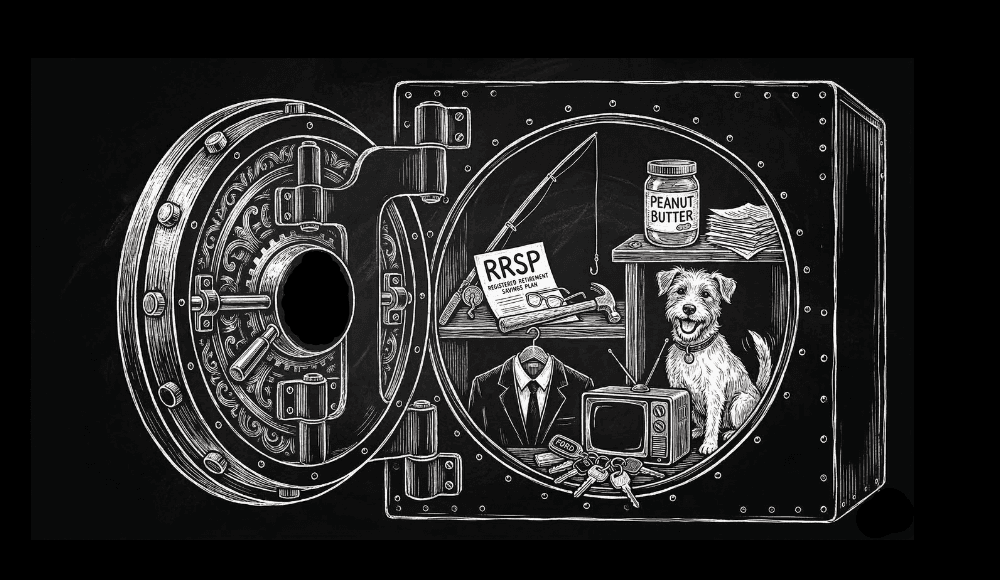

4. Your secured debts and assets remain untouched

Unlike bankruptcy, a consumer proposal does not transfer control of your assets to a trustee. You keep your home, your vehicle, and all your investment accounts. As long as you continue making payments on secured obligations like your mortgage or car loan, those creditors have no involvement in your proposal. This distinction surprises Canadians who assume that any formal insolvency proceeding means losing property.

5. A rise in income does not increase your payments

Once your creditors accept the proposal terms, your total repayment amount is locked in. If you receive a raise, a bonus, or a second source of income during the proposal period, your monthly payment stays the same. In a bankruptcy, surplus income triggers higher mandatory contributions. This fixed-cost structure is one of the most significant effects of a consumer proposal that filers only appreciate once their earnings improve.

6. Interest stops accruing on all included debts from the filing date

Every dollar you pay under a consumer proposal goes toward principal. On a $50,000 balance of credit card debt at an average rate of 20%, stopping interest saves thousands of dollars per year. Many filers are surprised at how quickly their proposal balance declines compared to years of making minimum payments where most of the money went to interest charges.

7. You can answer "no" when asked if you have ever been bankrupt

A consumer proposal is not bankruptcy. Employment applications, professional licensing forms, and volunteer screening checks that ask specifically about bankruptcy do not require you to disclose a consumer proposal unless the question explicitly mentions it. For Canadians in regulated professions or those who work with vulnerable populations, this distinction can protect career opportunities.

8. CRA debts, including personal income tax and HST, are included

The Canada Revenue Agency is treated as an unsecured creditor in a consumer proposal. Outstanding personal tax debts, interest, and penalties are swept into the proposal alongside credit card balances and lines of credit. CRA can no longer issue a Requirement to Pay to your employer or freeze your bank account once the stay of proceedings is in place. Many Canadians do not realize that tax debt, which otherwise carries aggressive collection powers, can be resolved this way.

9. Missing three payments annuls the proposal automatically

If you fall three months behind on your scheduled payments, the proposal is deemed annulled by law. Your debts are fully reinstated, creditors regain the right to pursue collection, and any amounts you already paid are not returned. This consequence is strict and automatic, so building a realistic budget before filing is essential. Your Licensed Insolvency Trustee will help you set a payment amount that accounts for your actual household expenses.

10. The credit bureau notation clears three years after you finish, not three years after you file

A consumer proposal remains on your Equifax and TransUnion credit reports for three years following the date you complete all payments and receive your Certificate of Full Performance, or six years from the date of filing, whichever comes first. Paying off your proposal early shortens the total time the notation appears. This is why some filers make lump-sum payments or accelerate their monthly schedule whenever they can.

Related Posts

View All

10 Surprising Items You Can Legally Keep Thanks to Canadian Bankruptcy Exemptions

Arguably the biggest misconception about Canadian bankruptcy is that you will automatically lose your car.

The Pros & Cons Of Declaring Bankruptcy in Canada

“I think filing for bankruptcy can prevent heart attacks, suicide, divorce, and job loss because people can now focus on life, as opposed to fighting with creditors they cannot afford to pay,” argues Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.

Consumer Proposal VS Bankruptcy: How To Pick The Best Option Based On Your Situation

A consumer proposal tends to serve you better if you have a steady income and assets you want to protect.