By Julien Brault, founder of MooseMoney.

If your Canadian bank account is frozen, you cannot withdraw money, make transfers, or receive deposits until the issue is resolved. The freeze may be caused by suspected fraud, unpaid debt owed to a creditor, or a tax obligation with the Canada Revenue Agency (CRA). Your first move should be to contact your financial institution immediately to confirm the freeze and understand exactly why it happened.

Under the Bank Act of Canada, three entities can freeze your bank account. Your bank can freeze it without a court order if it detects suspicious activity or fraud. A general creditor can freeze it after obtaining a court judgment against you for unpaid debt. The CRA can freeze your account without a court order and without advance warning if you owe unpaid taxes. The federal government also holds the power to freeze accounts in specific circumstances, including suspected terrorism or financial crimes.

Tim Morris, Chief Banking Officer at Neo Financial, recommends keeping calm and contacting your institution’s customer service. "If your account is frozen, reach out to customer service to get confirmation that your account is in fact frozen, because it could be a system failure or related to a hold, it could be something else. Specifically ask them what can be done to unfreeze the account or resolve the situation," said Morris.

What Happens When Your Account Is Frozen

When a freeze is in place, all account activity stops. You cannot make withdrawals, send e-Transfers, or use your debit card. Incoming deposits, including paycheques, direct deposits, and government benefits, are also held. Pre-authorized payments for your mortgage, utilities, car loan, or insurance will not go through, which can trigger missed payment fees and damage your credit score.

If the CRA issued the freeze through a Requirement to Pay notice, your bank is legally required to forward any funds in the account, up to the amount of your tax debt, directly to the CRA. Future deposits can also be captured and sent. The CRA may simultaneously issue a garnishment order to your employer, redirecting a portion of your paycheque before it even reaches your account.

There is no legal time limit on how long a bank account can remain frozen in Canada. A fraud-related freeze may last days or weeks while an investigation is completed. A CRA freeze can remain in place indefinitely until your full tax balance is paid or you file a consumer proposal or personal bankruptcy through a Licensed Insolvency Trustee (LIT).

What To Do Next

Contact your bank first. Get written or verbal confirmation of the freeze, the reason behind it, and the specific steps required to resolve it. If the freeze is fraud-related, your bank will initiate an investigation and may issue a new debit card or reset your credentials.

Open a new account at a different institution. If the freeze will take time to resolve, you need a new chequing account, preferably a no-fee one like the Neo Everyday account,to make sure you can cover your basic expenses. Then, redirect your payroll, direct deposits, and automatic bill payments to that account immediately.

Deal with the underlying cause. If a creditor froze your account, your bank should provide the creditor's contact information and the details of the judgment. Reach out to negotiate a payment plan. If the CRA froze your account, contact them to discuss repayment options. The CRA may accept an installment arrangement if you demonstrate a genuine effort to pay. If you disagree with a CRA assessment, you can file a formal objection within 90 days of the notice of assessment, and you can appeal to the Tax Court of Canada if the objection is denied.

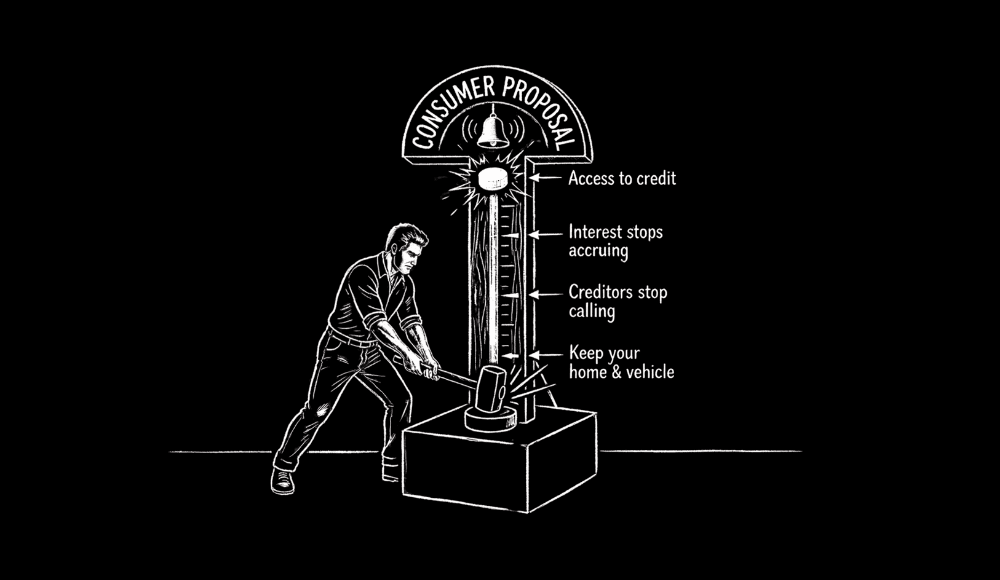

If you cannot repay, talk to a Licensed Insolvency Trustee. A LIT is a federally regulated professional who can help you file a consumer proposal or a personal bankruptcy. A consumer proposal triggers an automatic stay of proceedings, which stops all collection actions, including a bank account freeze. Personal bankruptcy also triggers a stay of proceedings but carries more severe consequences for your credit and assets.

What Not To Do

Do not ignore the freeze and assume it will resolve on its own. Frozen accounts typically result from escalated collection efforts after multiple attempts at contact, so the creditor or CRA is unlikely to release the hold without action on your part.

Do not attempt to move money out of a frozen account through workarounds. Once the freeze is active, the funds are locked and any attempt to circumvent that can complicate your situation.

Do not wait until your account is frozen to deal with outstanding debts or tax obligations. If you are behind on payments to the CRA or any creditor, contact them proactively to set up a payment plan. Addressing the issue before it escalates to a freeze gives you far more negotiating leverage and avoids the disruption of losing access to your primary bank account.

Related Posts

View All

How Do I Stop Automatic Payments In My Bank Account in Canada

If an unauthorized payment has already been withdrawn, you have 90 days to file a reimbursement claim under Payments Canada's PAD rules.

Does the Canada Revenue Agency (CRA) Know About All My Bank Accounts?

The short answer is no, the CRA does not automatically know how many bank accounts you have or see the transactions flowing through them.

10 Unexpected Effects of Doing a Consumer Proposal in Canada

Unlike bankruptcy, a consumer proposal does not transfer control of your assets to a trustee. You keep your home, your vehicle, and all your investment accounts.