Published on June 1, 2026 · 4 min read

By Jason Heath, fee-only financial planner and managing director at Objective Financial Partners

As told to Jessica Martel.

From our sponsor

Here’s the answer to this week’s reader question.

I wanted to get a loan. But can I use a credit card to pay my college fees? Please, is there anything else that can help me with my student debt?

–Aman

Can you pay for tuition and school fees with a credit card in Canada?

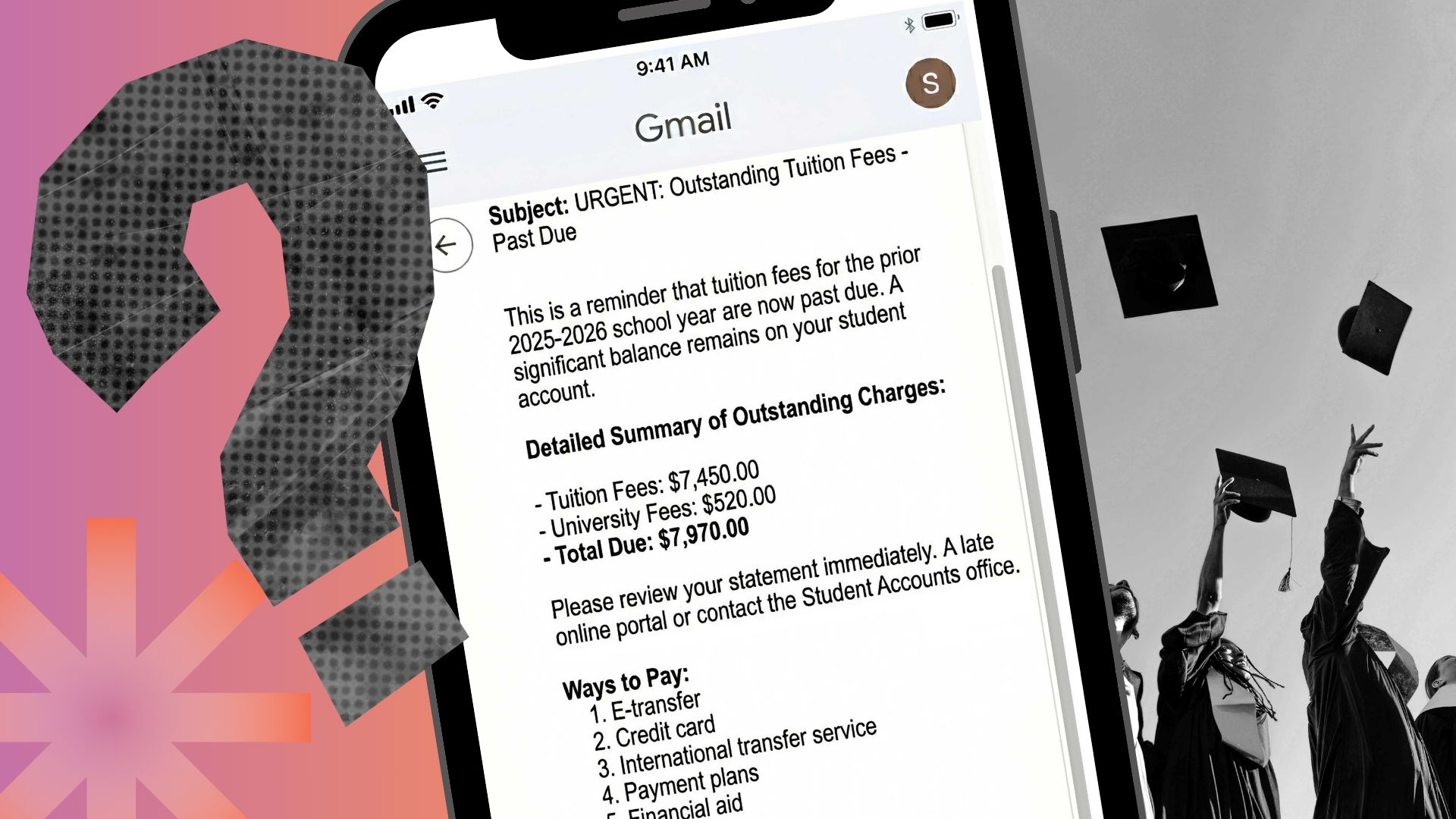

Going to college is an exciting milestone, but figuring out how to pay for it can be a heavy workload. The average cost of tuition for an undergraduate degree in Canada is $7,734 per year. Like many students, you may need help covering tuition and expenses and you may also wonder if you can use your credit card as a quick and convenient solution.

Can I use a credit card to pay my college fees?

In some cases, you may be able to use a credit card to pay your college fees and tuition, but it depends on your school. Colleges or universities that accept credit card payments may charge a processing fee, which is usually around 2.5%. If you’re paying the average tuition of $7,734 per year, that’s $193.35 in processing fees.

Some post-secondary schools in Canada only accept credit card payments through third-party service providers like Chexy. Since each college or university has its own policy, it’s best to contact the registrar’s office or the financial services department directly to confirm whether you can pay with your card and what the cost will be.

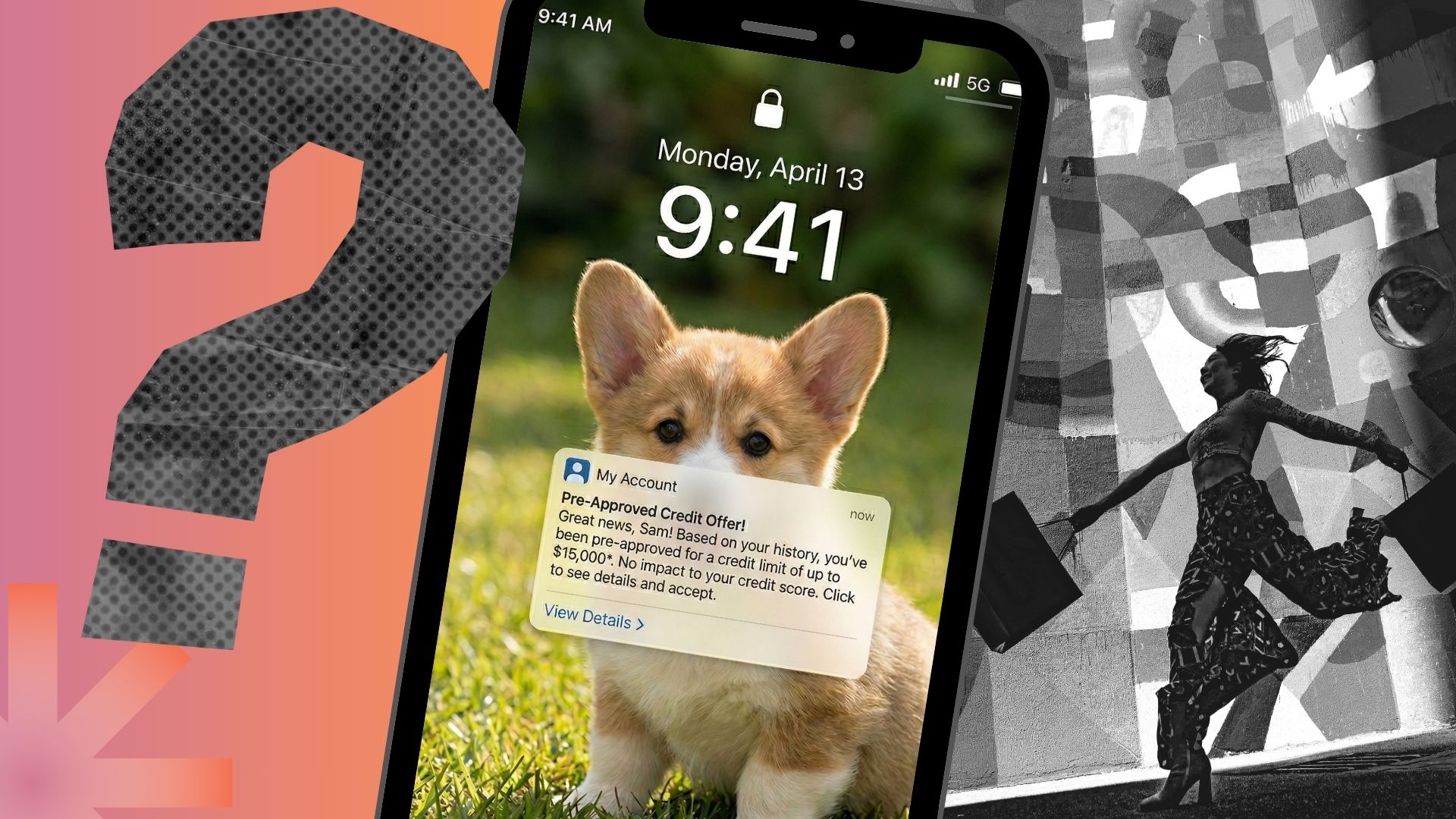

Even if it’s possible to pay with a credit card, this doesn’t mean you should.

Yes, it’s convenient and may even earn you rewards, but carrying a balance becomes problematic when you don’t have regular income. With interest rates reaching 20% or more, paying with your credit card can be costly—much more than other lending options. So, if you can’t pay your balance immediately, this isn’t the best approach.

What are other options to pay for college?

So, if your credit card isn’t the best option, what are some other ways you can pay for college? A good place to start is with government student loans. You’ll need to submit an application through the student aid program. You only have to submit one application to be considered for both provincial and federal loans. Once you apply, the aid office will reach out with next steps. With student loans, you generally have to start repaying them six months after you finish school, but you don’t need to repay government grants.

If you have no income or you’re struggling financially when you’re supposed to start repaying your loans, you can apply for the government Repayment Assistance Plan (RAP). Based on your income, you may qualify to have your payments reduced or removed. You can apply to the RAP program any time during your repayment window and you have to reapply every six months to stay eligible for assistance, based on your financial situation. After you’ve been on RAP for 60 months or you’ve been out of school for 10 years (whichever comes first), the government will start to pay off your remaining balance.

As of April 2023, the Government of Canada removed interest payments on the federal portion of student loans. Many provinces, including British Columbia, Manitoba, Nova Scotia, New Brunswick, Prince Edward Island, and Newfoundland and Labrador have also eliminated student loan interest. Alberta, Saskatchewan and Ontario still charge interest but offer competitive rates that are based on the Bank of Canada’s prime rate. As of early 2026, the prime rate is 4.45%. To put this in perspective, the average interest rate on a car loan is around 7% and on a standard credit card is 20% or higher.

If you miss the deadline to apply for student loans or you don’t qualify, you still have other options, including:

- RESP: You can withdraw funds from your registered education savings plan (RESP) if your family has contributed to one.

- Scholarships: Apply for scholarships and bursaries through your school’s financial aid office or online databases. This is money that you don’t have to pay back.

- Student line of credit: With a line of credit, you can borrow money from a bank or financial institution up to your credit limit and access those funds again as you repay the money. You only pay interest on the money you use, but you have to pay at least the interest while you’re still in school.

- Part-time work: Finding a job or participating in a co-op program where you can earn money can also help you cover your costs.

So, while you can pay for school with a credit card, know that you have other options.

Jessica Martel, MSc is a freelance writer, researcher, and certified financial education instructor (CFEI). She is based in Calgary, Alberta.

Read more from this issue of The Get:

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.