Published on April 13, 2026 · 4 min read

By Mark Kalinowski, CEPF, financial educator with the Credit Counselling Society

As told to Ian Portsmouth

Here’s the answer to this week’s reader question.

What is pre approved credit?

—Sam

What is pre-approved credit?

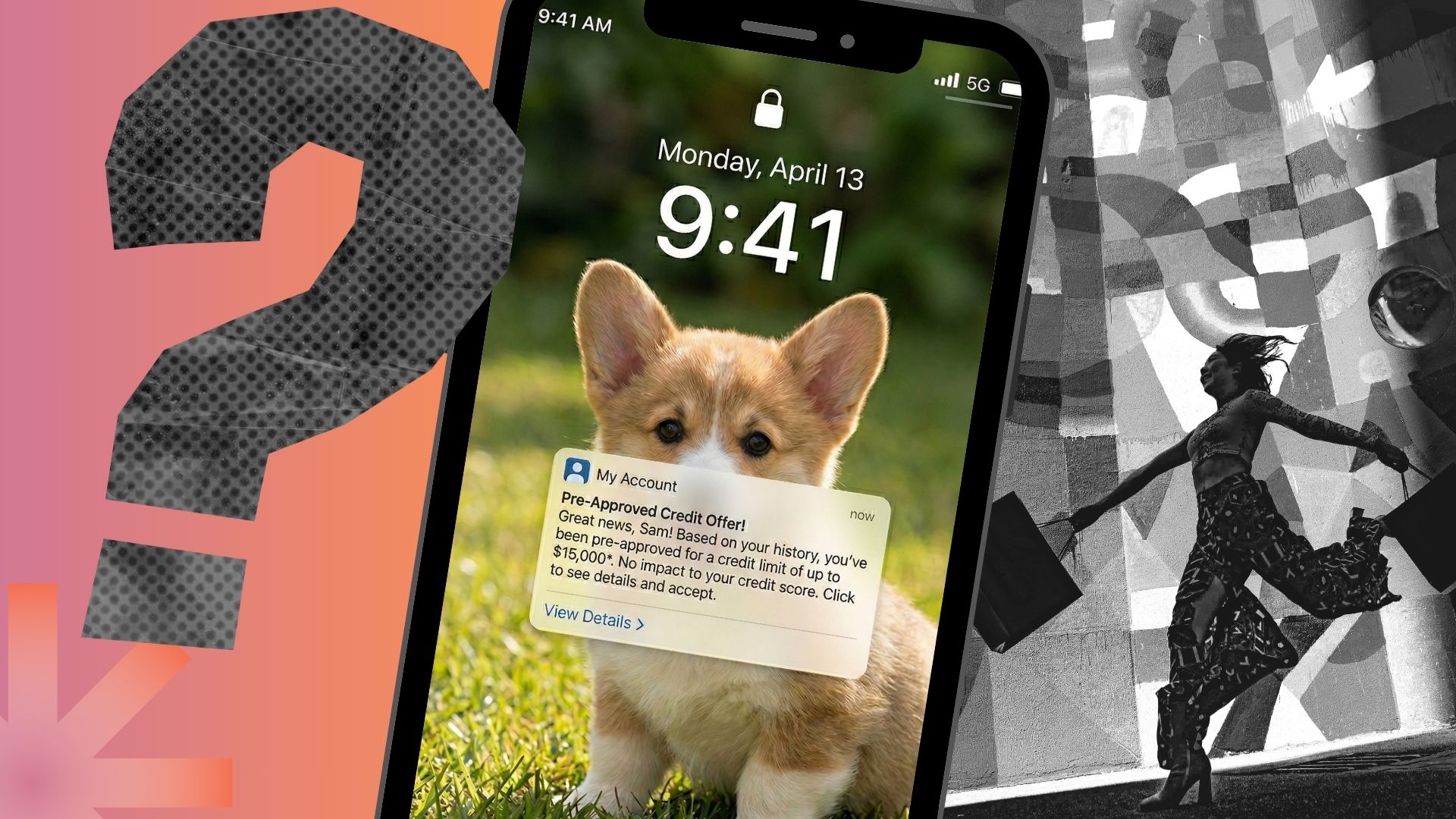

Most people get introduced to the concept of pre-approved credit when their financial institution offers it to them, usually by mail, email or a notification in their banking app. These offers are a form of marketing designed to invite existing or potential customers to obtain a credit product, such as a credit card or a line of credit, or accept a higher borrowing limit on an account they already have.

Does pre-approval mean you’ve been approved?

Despite its name, a pre-approved credit offer doesn’t necessarily mean you’ve been approved for a loan or a credit card. Rather, it’s a targeted invitation to apply for credit, sent to people who the financial institution believes may be a good candidate for the financial product.

The institution determines this with a “soft” check of your credit, which doesn’t affect your credit score, or by analyzing detailed information it already has on file. If the results suggest you’re likely to qualify for the product, it may send you an offer saying you’ve been pre-approved.

Typically, responding “yes” to one of these offers starts an application process. The lender may ask for information, such as your annual income, and may ultimately do a “hard” credit check, which will be recorded on your credit report and may temporarily affect your credit score. After this review, the financial institution will make its final decision to approve or not. In that sense, a pre-approved credit offer is better understood as a conditional offer: you aren’t approved until you meet all the lender’s requirements.

Sometimes, however, pre-approved credit is exactly as presented: accept the offer and you receive the credit, without providing additional information or being subjected to a hard credit check.

Offers like these usually apply to increases on borrowing limits on credit cards or lines of credit you already have, because the financial institution can gauge your creditworthiness from your account activity and other information it has about you. Still, the underlying logic is similar: the institution has assessed you in advance and decided you are a good risk for additional credit.

How mortgage pre-approvals differ

Pre-approved mortgages are different from other forms of pre-approved credit, however. Despite sounding similar, a pre-approved mortgage is initiated by the borrower rather than the lender. Essentially, it’s a time-limited guarantee from a lender that a potential homebuyer is eligible for a mortgage of a specified size at a specified interest rate, allowing the homebuyer and seller to negotiate a deal with confidence that financing is in place.

Of course, the mortgage pre-approval process is rigorous, involving a full application, documentation of income and debts, a hard credit check and a thorough assessment by the lender.

Should you accept a pre-approved credit offer?

You shouldn’t accept pre-approved credit just because it’s offered. You need to be able to use it responsibly within the context of your financial situation, not to spend beyond your means.

There are a couple of strategic reasons to accept a pre-approved credit offer. One is to increase your available credit in the event of an emergency. The other is to increase your credit score because the additional credit will give you a lower credit utilization ratio, which is better for your credit score—at least temporarily. In both cases, the key is to accept the credit without using it for the wrong reasons.

As noted your acceptance may trigger a hard credit check, which may count against your credit score for the three years it can stay on your credit report.

Accepting more credit can work against you when seeking a large loan, like a mortgage. It’s standard for lenders to test your ability to paying toward all your actual debts with your current income. But some more conservative lenders will compare your income to your total available credit. In other words, they consider what your debt would be if you used up 100% of the credit available to you. So, accepting a pre-approved credit offer today could, ironically, lead to rejection tomorrow.

You should also consider the terms of the credit itself. For instance, some pre-approved credit is promoted with a low introductory interest rate that jumps to a higher rate when the promotional period expires. And offers to transfer your existing credit card balances to a new pre-approved card usually come with transfer fees of 1% to 3% of the transferred balances.

Whenever considering any new credit product, read the full terms and conditions to learn about different interest rates for different types of usage (e.g., purchases versus cash advances), penalties for missed payments, and more.

Is pre-approved credit a good thing?

A pre-approved credit offer is just that—an offer. It doesn’t obligate you to say yes, and it doesn’t guarantee that you’ll receive the credit. Your decision should come down to whether the product fits your needs, whether you understand the terms and risks, and whether you can manage it comfortably over time.

Ian Portsmouth is an award-winning writer and editor specializing in business and personal finance. He is based in Toronto.

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.