Your 20s are an interesting time. You’re likely finishing school and are looking at the next chapter of your life, trying to figure out what to prioritize. You want to have fun, but also set up your future self for success. You might even be a little angry that school taught you more about trigonometry than personal finance.

Luckily, it’s never too late to learn new things. We’ve compiled a list of the top nine things you should start thinking about before you’re 30.

1. Improve your financial literacy

As we alluded to earlier, our education system doesn’t adequately equip you for understanding and navigating personal finances. But hey, the mitochondria is the powerhouse of the cell, right?

Now is the perfect time to start improving your financial literacy and delve into the world of personal finance. We believe that knowledge is power, so the more you know the more empowered you are to make informed decisions.

Improving your financial literacy will also help you more confidently navigate important life decisions like your first career job after graduation, buying a house, and maybe even getting married and having kids. Learning how to better understand money now can set you up for a lifetime of success with your finances, and help you avoid the pitfalls.

Besides staying up-to-date on our blogs, there are many other tools to level up your knowledge. We’ve pulled together some favourites from books to YouTube channels, but you can learn almost anywhere. If you’re like most 20-year-olds, you’re probably on Tik Tok—so let that algorithm know you want to be on #fintok and start learning there too. Even just 10 minutes of learning a day can help you get ahead.

Books

#1: Financial fundamentals

Why Didn't They Teach Me This in School?: 99 Personal Money Management Principles to Live By - Cary Siegel

If you’re just getting started in the world of personal finance, Cary Siegel walks you through the most fundamental lessons. These are things you should have learned by the time you graduated from high school or post secondary, but possibly didn’t. Siegel breaks down themes and lessons into digestible sections that make it easier to learn from.

#2: Budgeting and debt management

Broke Millennial: Stop Scraping By and Get Your Financial Life Together - Erin Lowry

From budgeting and debt management (hello student loans), to negotiating your salary and investing, this book covers a lot of the basics you’ll want to start learning in your 20s. Lowry brings a light tone as she discusses the #millennialstruggle and helps educate in a way that doesn’t just discourage avocado toast. Note: this book is written from an American perspective and some terms might not cross over into Canadian banking.

#3: Relationship with money

I Will Teach You to Be Rich, Second Edition: No Guilt. No Excuses. No BS. Just a 6-Week Program That Works - Ramit Sethi

This New York Times and Wall Street Journal bestseller will change your relationship with money. Ramit uses his psychology background to teach you how to spend smart, automate saving and investing, buy a house, and even how to talk yourself out of late fees. Note: this book is written from an American perspective and some terms might not cross over into Canadian banking.

Podcasts

#1: The MapleMoney Show

Founded by a Calgarian financial analyst, Tom Drake, the Maple Money Show can walk you through countless topics that are relevant in your 20s and beyond. This podcast covers subjects such as financial independence, NFTs, loans, credit, and so much more.

#2: More Money

With over 300 episodes and 2.5 million downloads, this is one of the biggest Canadian financial podcasts. Jessica Moorhouse interviews celebrities, entrepreneurs, authors, friends, and even listeners to discuss all things finance. Want to know how much it really costs to own a pet? There’s an episode for that. Looking for something a bit deeper? Listen to the episode on trauma, privilege, and diversity in personal finance.

#3: Moolala: Money Made Simple

Bruce Sellery is the CEO of Credit Canada and spent years as a business journalist, financial literacy consultant, and personal finance expert. His podcast covers numerous topics you’ll find yourself asking about in your 20s: your relationship with money, spending at restaurants, inflation, the finances of content creation, socially responsible investing, and much more.

Youtube

#1: Steph & Den

This YouTube channel is hosted by two 20-something Torontonians that create content to help young adults grow in their careers and generate more disposable income. They cover essential topics like investing, saving, budgeting, and buying a home. They present their take on many of the financial topics and dilemmas you’re likely to encounter in your 20s.

#2: The Financial Diet

Explore real discussions around many of the toxic mentalities surrounding financial culture. That 5 a.m. “billionaire routine”? They tried it and let you know their thoughts. They also explore “toxic boomer” money advice that you need to let go of, resume do’s and don’ts, and even habits you might have adopted if you grew up with financial instability.

#3: MappedOutMoney

Nick True walks through various personal finance topics that you’re bound to run into during your 20s. How to buy a house in this market? How to stay calm and prepare financially during a crisis? How to allocate extra money? He even takes time to debunk the myth that cutting your morning coffee will drastically improve your savings.

2. Start budgeting

You probably know what budgeting is, and maybe even roll your eyes or cringe when you see the word. It might be a tedious and annoying task, but it can really help you organize your money and financial priorities.

Budgeting isn’t about not spending your money, it’s about how you spend your money.

If you can break down your average monthly income and expenses (rent, bills, subscriptions, etc.), you can see how much money you have to put towards things you enjoy.

Make a budget that works for you and fits your priorities. If you don’t and your budget is just a monthly scolding then you’re not going to want to keep using it, are you? So set up a budget that is realistic but as simple or complex as you want.

- Simple: put aside money for your expenses and savings each month and then spend the rest of your money as you want.

- Complex: map out all your fixed expenses, and budget out how much you want to spend on essentials like groceries, gas, etc. Then budget how much of your income you want to go towards clothes, social activities, savings, etc.

With proper budgeting, you won’t have to stress about guac being extra. If your budget allows for it then treat yourself. Budgeting helps you make informed decisions when it comes to spending your money, and even takes the guilt out of spending money on things you want.

If you haven’t used a budgeting tool before, Nerd Wallet points out their favourite budgeting apps. The list has a variety of options and pricing (yes, including free options) that can fit your needs.

3. Know the difference between an RRSP and TFSA

RRSP stands for Registered Retirement Savings Plan. This is a government-sponsored retirement plan you can set up through your bank or other financial institutions. RRSPs were created to help motivate people to save for retirement through tax incentives: money that is placed in your RRSP is exempt from income taxes until you withdraw the funds.

RRSPs limit how much you can place into the account each year (contribution limits). This limit is unique to each individual and is based on factors like when you start earning income, deposits from previous years, etc. This contribution limit impacts how much you can deduct off your taxes for that given year. That being said, there are very strategic ways people use their RRSPs to maximize the benefits.

A TFSA is a Tax-Free Savings Account. Many people use their TFSA for investments since the profit you generate using it won’t be taxed. It’s not great for using as a traditional “savings” account, since it doesn’t automatically incur any interest; however, it’s great for investing. This can help incentivize people to find other ways to save for their future beyond savings accounts that offer .005% interest.

Similar to the RRSP, there are limits on how much you can contribute to your TFSA each year, also known as a contribution limit. This is again a unique number and can vary year to year. You can also withdraw funds from your account as you please without paying any taxes (contrary to the RRSP).

4. Build your credit score

Have you checked your credit score recently? If not, do a quick check on Intuit Credit Karma or Borrowell to see where you stand. The average credit score for people in their 20s is just under 700, so if you’re in that range you’re doing great. If you’re below that, no problem, here are some tips on improving your credit score.

Building your credit score while you’re young is one of those small things that can have a big impact on your financial future. Having great credit helps you secure future credit (car loan, mortgage, etc.) and can help you get lower interest rates (why spend more if you don’t have to?). It can even help you find better home rental options and insurance rates.

5. Build an emergency fund

A lot of unexpected things happen in life, and it really sucks when emergencies put stress on your finances. An emergency fund can help reduce stress if you’re faced with vet appointments, car troubles, job loss, or other unexpected life events.

How much should you set aside for emergencies? Saving the equivalent of 3–6 months of your monthly expenses is great. Others recommend working towards 3–6 months of your monthly salary, which can be hard in your 20s on top of other things to be saving for, but hey it’s all one step at a time.

Pro Tip: Save your emergency fund in a high-interest savings account to earn interest on every dollar saved!

6. Plan debt repayment

Whether it’s a credit card, car loan, student loan, or something else, most people carry some sort of debt in their 20s. First and foremost, let’s be clear, carrying debt is not an inherently bad thing. Debt is pretty much unavoidable, and there can be some great ways to leverage debt to your benefit.

That being said, too much debt can feel overwhelming. Your 20s can be the time you start transitioning from student loans to a mortgage or other financial priorities. Paying off debt helps reduce stress and allows you to reallocate your money, plus cut down on the interest you’re paying.

Carrying multiple accounts with debt can feel impossible to pay off or keep track of. Here are some questions to consider while you plan:

- Where do your payments fit within your budget?

- What debt repayment techniques do you want to use?

- How quickly do you want to pay it off, and how does that affect your monthly payments?

- Which accounts have the lowest balance?

- Which accounts have the highest interest rates?

Note: Paying only the minimum monthly payment on your accounts means you’re ultimately paying more interest in the long run. That’s why paying off debt faster saves you money.

We have a great debt management resource: Understanding debt: making a debt management plan that works for you.

7. Pay off debt

How can you work towards paying off any outstanding debts faster? How can you avoid interest? How can you stay motivated? There are two main methods for paying off debt faster: debt stacking (or avalanching) and debt snowballing.

Debt Stacking / Debt Avalanching

This technique is about focusing on paying off debts with the highest interest rates first. In this method, you would pay off more than the minimum balance on the account with the highest interest rate, while also paying the minimum balance on your other accounts. This helps you to spend less money on interest overall.

Let’s look at an example: Say you have a credit card with a 20% interest rate, a car loan with a 5% interest rate, and a student loan with a 2% interest rate. Which one would you focus on paying off first with this method? You would first pay off your credit card, then the car loan, and then the student loan.

Debt Snowballing

This technique focuses on paying off the smallest debts first to build momentum towards paying off your largest debts. Here you would use extra cash to pay off the smallest debts first, while also paying off the minimum balances on your other accounts. This method does mean that you could end up paying more in interest; however, it also makes you feel good as you pay off your smaller debts more quickly, motivating you to keep working towards debt repayment.

These are two great methods for debt repayment, and when it comes to choosing between the two, it really comes down to personal preference. As long as you’re making the minimum monthly payments on all of your accounts with a plan that works for you, you’re making good progress while preserving your credit score.

8. Save for a down payment

Okay, we’ve talked about education, budgeting, credit scores, emergency funds, and paying off debt—but we still need to discuss saving in your 20s.

When there’s so much going on, it’s hard to think about saving for something other than that trip to Europe, but it’s always a good idea to think about longer term goals, like a down payment on a home, or even retirement.

For those of you who are looking at buying your first home, it can feel daunting and intimidating. At this stage of life, your first home is likely the largest financial decision you’ll make. You take one look at the soaring housing prices and it feels unattainable, doesn’t it?

It might help to keep in mind that you only need 5% for a down payment on a home. You can also look at smaller properties and create a plan to build equity and work your way up the real estate ladder. With any big and intimidating goal, breaking it into smaller more achievable milestones can go a long way in helping you achieve them.

While you can go as low as 5% for a down payment on a house, if you can swing it, there are some upsides to putting down 20%:

- You'll pay less interest overall on your mortgage,

- You’ll pay less mortgage default insurance (CMHC), and

- Your monthly mortgage payment will be more affordable

Even if you don’t plan on getting a mortgage for a home until your 30s, starting to set aside funds in your 20s can make this goal more attainable and less stressful.

Ultimately, figure out what fits in your budget and what you’re comfortable saving and start following through. Even placing $20 a month into an account to get in the habit of putting money aside for a home can be helpful. Then you can review and reprioritize your budget as your financial situation changes.

9. Start retirement planning

Who wants to start thinking about retirement in their 20s? Well, anyone who’s in their 40s that didn’t. But in all seriousness, when you start investing in your retirement, even just a little, you make it so much easier for yourself in the long run with compounding interest.

With compound interest, the amount in an account earns interest, then the total amount including the interest already earned will continue to earn even more interest. In this way, the interest is reinvested rather than paid out. This helps your money grow significantly faster.

In fact, Business Insider breaks down that you can earn almost double your savings by starting at 25, rather than at 35.

Conclusion

If you’ve read this far, you might be stressing out a little. That’s okay. Start small, keep educating yourself, start planning, and you’re going to set yourself up for success.

Take some time to set your goals and revisit them every 6 months. You’ll find that your finances are going to look a lot different over time. Create a plan that works for you and your goals now, and adjust them as life evolves.

Legal:This article provides information and is not intended to provide any personalized tax, investment, financial, or legal advice. You are encouraged to seek professional advice before making financial decisions.

Related Posts

View All

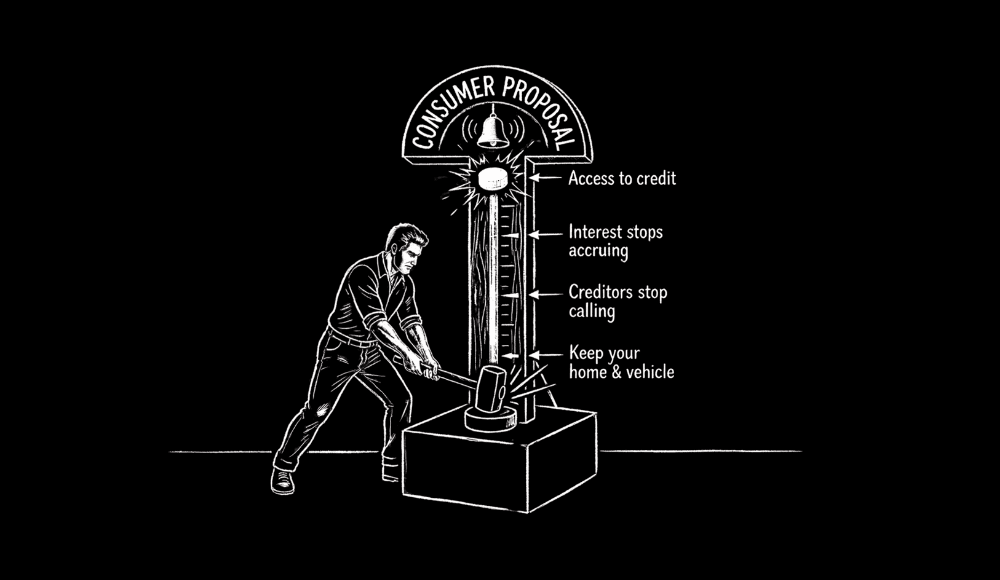

10 Unexpected Effects of Doing a Consumer Proposal in Canada

Unlike bankruptcy, a consumer proposal does not transfer control of your assets to a trustee. You keep your home, your vehicle, and all your investment accounts.

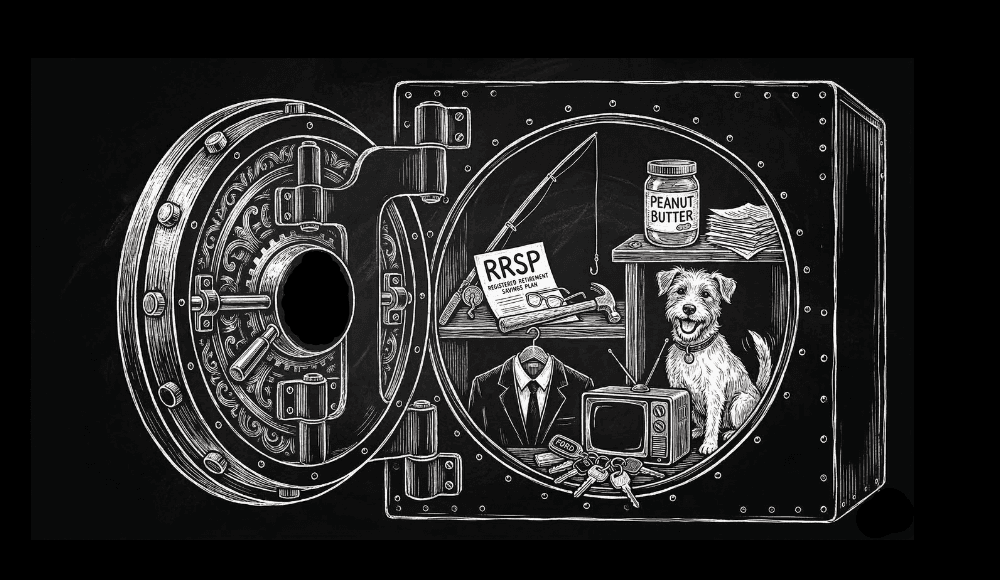

10 Surprising Items You Can Legally Keep Thanks to Canadian Bankruptcy Exemptions

Arguably the biggest misconception about Canadian bankruptcy is that you will automatically lose your car.

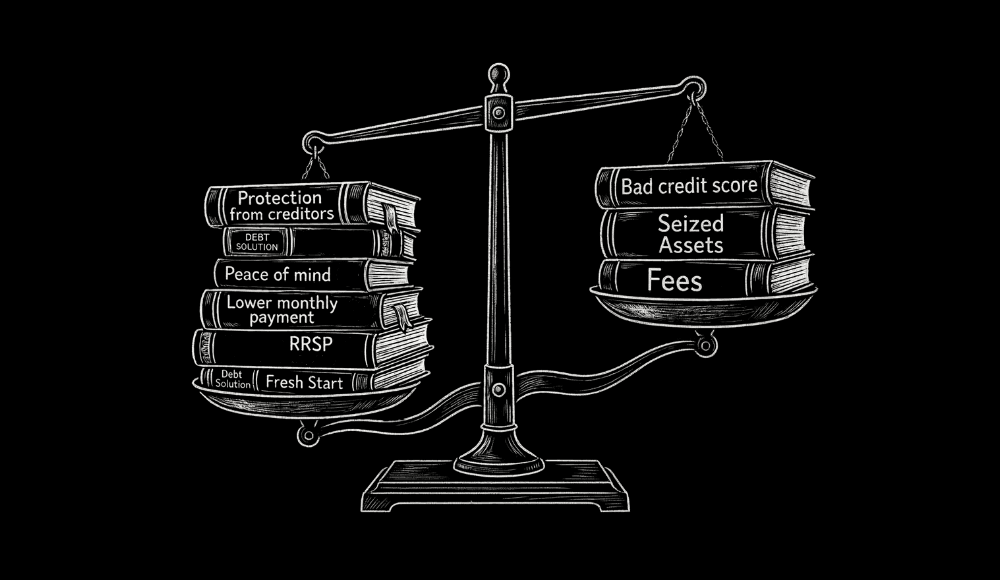

The Pros & Cons Of Declaring Bankruptcy in Canada

“I think filing for bankruptcy can prevent heart attacks, suicide, divorce, and job loss because people can now focus on life, as opposed to fighting with creditors they cannot afford to pay,” argues Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.