Published on March 26, 2026 · 5 min read

By Julien Brault, founder of MooseMoney.

When you arrive in Canada, your credit history does not come with you. Regardless of how responsibly you managed debt in your home country, Canadian lenders, landlords, and even some employers will see a blank file. The fastest way to start building credit from scratch is to get a secured credit card, use it for small recurring purchases, and pay the balance in full every month. Within six to twelve months of consistent on-time payments, you will have a usable credit score.

Richard Goyder, Chief Credit Risk Officer at Neo Financial, has experienced this firsthand. "I had a perfectly good credit rating back home in the UK and when I moved to Canada, I had no credit rating at all. I was married to a Canadian, so I could rely on my wife's credit rating, but I had none of my own," explained Goyder.

Going From No Score To Good Score

Canada's two national credit bureaus, Equifax and TransUnion, each maintain a file on you once a lender first requests your report. "Once the first attempt to pull a credit file that doesn't exist occurs, that credit file gets created. Now, the person does have a credit report, but not a credit score," stated Julie Kuzmic of Equifax Canada.

At Equifax, a credit score will only appear after enough payment data accumulates, which typically takes three to six months of reported activity. At TransUnion, newcomers get attributed a credit score almost instantly, although it will typically be on the low end due to the lack of history.

Canadian credit scores range from 300 to 900. A score of 300 is not your starting point as a newcomer because that number is reserved for people with a documented history of missed payments and defaults. If you use credit responsibly from day one, your first calculated score should land well above the floor. "If the person has been paying on time each month, then I believe that it would typically start quite a bit higher than 300, which is the lowest possible score that can be calculated," explained Julie Kuzmic, Head of Consumer Advocacy and Compliance at Equifax Canada.

Your score is shaped by five main factors: payment history (the most heavily weighted), credit utilization ratio, length of credit history, types of credit, and recent credit inquiries. Because the length of your history matters, building credit is not instant. "If you open up a secured card with Neo and use it sensibly, you will improve your credit score. But because a large part of what goes into your credit score is the history, it takes some time," stated Goyder.

Why Your Foreign Credit History Usually Does Not Transfer

Canadian credit bureaus do not pull data from bureaus in other countries. A company called Nova Credit offers a product called Credit Passport that translates international credit files for participating lenders. However, adoption across the industry remains limited. "What Nova Credit does is it gives banks and issuers access to people's foreign credit bureau. Neo does not use it and I don't think many Canadian lenders use it," said Goyder. For most newcomers, the practical reality is that you will need to build a Canadian credit file from zero.

Step-by-Step Plan to Build Credit From Scratch

1. Get a Social Insurance Number first

You need a SIN to open credit accounts in Canada. You can apply online or in person at a Service Canada Centre.

2. Open a chequing account

A basic bank account like the Neo Everyday Account does not generate a credit score on its own, but it establishes a relationship with a financial institution and gives you a place to manage bill payments.

3. Apply for a secured credit card

A secured card requires a refundable security deposit, and your credit limit typically equals that deposit. The Secured Neo Mastercard, for example, reports your payment activity to the credit bureaus, while allowing you to earn cash back on your purchases.

4. Use the card for small, recurring expenses

Put groceries or a streaming subscription on the card and pay the full statement balance before the due date every month. Keep your utilization below 30 percent of your credit limit.

5. Avoid the interest trap

Richard Goyder, Chief Credit Risk Officer at Neo Financial, warns newcomers against a common pitfall like getting a high interest car loan just to build their credit. "The biggest mistake new immigrants can make when trying to build their credit history is accepting a very high interest rate loan. They're much better off getting a secured card, using it and making regular payments. It will be far more effective than having a single loan that could end up costing you thousands in interest," said Goyder.

6. Get a cell phone plan on a postpaid contract

Most major Canadian telecoms report payment activity to the credit bureaus. A plan under $60 per month keeps costs low while adding another tradeline to your file.

7. Consider rent reporting

Services like Borrowell's Rent Advantage can report your monthly rent payments to Equifax, adding another positive data point to your history.

How to Verify Your Progress

Not every payment you make gets reported to the bureaus, so checking your file is essential. Julie Kuzmic from Equifax Canada put it plainly: "The most important part of building credit is making sure that your positive payment history is being reported to the credit bureaus and the reality is that not all credit or bill payments are reported to credit bureaus. One way to make sure you are making progress is to take a look at your credit reports at both Equifax and TransUnion, which you can do for free."

You can access your credit report from both Equifax Canada and TransUnion Canada for free online. You can also monitor your TransUnion score on an ongoing basis through the Neo app through Neo's Build membership.

Related Posts

View All

Does Getting Your Rent Payments Reported to Credit Bureaus Actually Help You Build Your Credit in Canada?

Over the last few years, various rent reporting services have emerged in Canada, most of which only report rent payments data to Equifax. That includes Borrowell Rent Advantage, FrontLobby, and KOHO. More recently, rent reporting company Zenbase anno

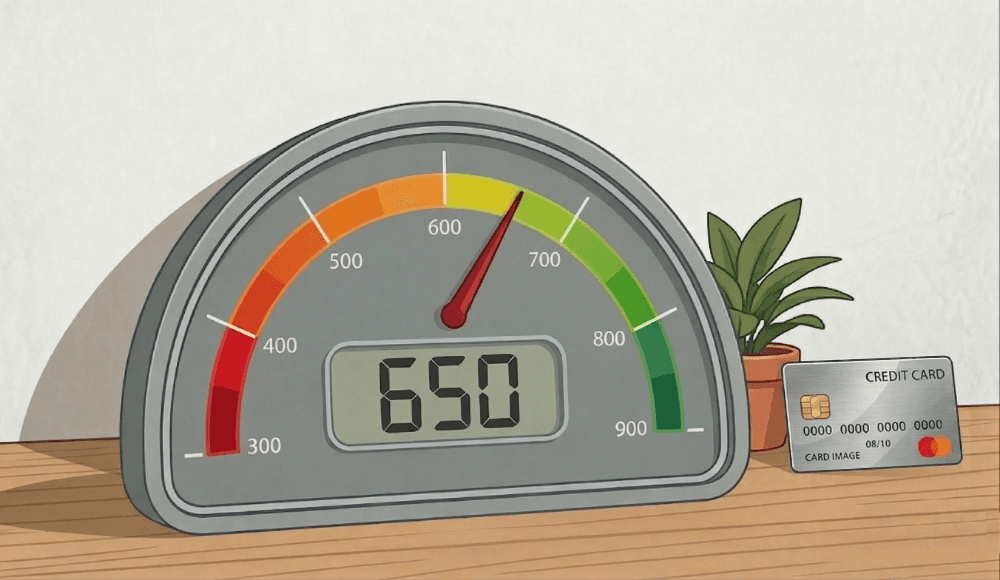

What You Can and Can't Do With a 650 Credit Score in Canada

You can still qualify for car loans, high interest personal loans, and secured credit cards, but you will face higher interest rates.

How to Freeze Your Credit and Avoid Credit Fraud in Canada

"If you're concerned about people opening up credit in your name or if your info were part of a leak, freezing your credit file is something you should consider."