Updated on July 6, 2026 · Published on April 14, 2026 · 4 min read

Managing money together should make your life easier, not add to your to-do list. When you open a joint account with a co-applicant, you aren’t just sharing cash—you’re actively taking a step towards streamlining bills, eliminating endless e-Transfers, or tracking your shared goals.

If you’re looking for the basics of a joint account—what they are, how they work, or whether it’s right for you—check out our guide to joint accounts in Canada.

But if you’re ready to take the next step and learn the steps to set your account up today, keep reading. This guide breaks down exactly how to open a joint bank account in Canada to help you fast-track your shared financial milestones.

From our sponsor

One common misconception is that joint accounts are only for married or common-law couples. Tim Morris, Chief Banking Officer at Neo Financial, clarifies, “In Canada, most financial institutions allow joint accounts between any two individuals, regardless of their relationship.” That means roommates splitting rent, parents helping a teenager learn to budget, or siblings pooling funds for a family gift can all hold a joint account together.

Joint account requirements in Canada

Opening a shared account in Canada is straightforward. Modern digital platforms like Neo have eliminated the need to visit a physical bank branch together.

Make sure both applicants have these standard details ready to easily open a joint bank account online:

- Personal identification: Valid government-issued ID, like a Canadian driver’s licence or passport for each person.

- Personal details: Full legal names, current addresses, phone numbers, and dates of birth.

- Tax residency status: Canadian Social Insurance Numbers (SIN) for tax reporting on any interest earned.

How to open a joint bank account online in Canada

Ready to get started? Here's how to open a joint bank account in Canada, step by step.

1. Choose your platform and account type

The financial institution you choose shapes how you manage your money daily. Legacy banks often require you to coordinate schedules and visit a physical branch together just to sign paperwork, but choosing a modern digital option like Neo cuts out the hassle. Processes are seamless and monthly fees are cut out of the equation.

You can match your account type to your goals:

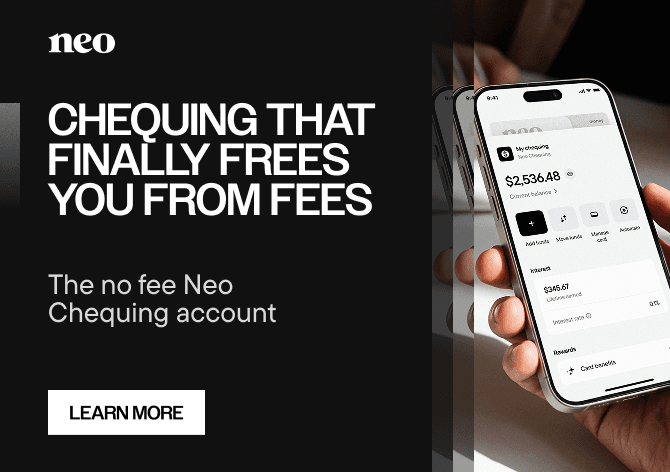

- For everyday expenses: A joint Neo Chequing account allows you to track shared spending instantly with real-time notifications. Learn more about how a joint chequing account in Canada works.

- For shared growth: Combining your funds in a high-yield joint Neo Savings account allows your money to work harder.

2. Customize your account

Managing shared money doesn’t have to feel like boring admin work. Modern platforms let you personalize your financial dashboard to match your life. When you set up your joint space with Neo, you can customize the account with a unique name and avatar—keeping your collective goals visual, organized, and distinct from your personal funds.

3. Verify your information

With Neo, you can complete your identity verification entirely from your phone. Once you submit the standard personal details and info listed in the requirements section above, you will be prompted for a quick verification check to help keep your account secure.

What if your co-applicant is not a Canadian resident?

You can open a joint account with a non-resident if they meet the standard onboarding requirements. These include a Canadian SIN and a verifiable identity document. For specific details on eligibility, review the joint Neo Chequing FAQs.

4. Fund your account

Once your identities are confirmed, you are ready to fund your account. If you want to maximize your everyday cash flow, look for options that give you complete utility. Choosing one of the best no-fee joint bank accounts in Canada means you can pay bills, send free Interac e-Transfers payments, and automate your pre-authorized household withdrawals—all without worrying about fees or minimum balance penalties.

5. Order your physical card

If you have a joint Neo Chequing account, both you and your co-owner can add your digital card to Apple Pay or Google Pay upon approval. You can also request a physical Neo Money™ card. This ensures you can both make seamless point-of-sale purchases, track individual spends under a single statement, and manage daily spending effortlessly.

Ready to open a joint bank account online?

Whether you're combining finances with a partner, splitting expenses with a roommate, or pooling funds toward a goal, navigating shared finances should feel easy.

The joint Neo Chequing account is built for this purpose: no fees, instant spending notifications for both account owners, and a seamless online setup. Two people, one account, zero branch visits.

Open a joint Neo Chequing account today.

By Julien Brault

Julien Brault is a fintech entrepreneur and personal finance expert dedicated to making financial literacy accessible to all Canadians. As the founder of MooseMoney, he currently focuses on helping individuals navigate financial struggles through actionable advice and financial calculators.

Related Posts

View All

Should you open a joint chequing account? Here’s what you need to know

Learn how a joint chequing account works in Canada, who can open one, and how the joint Neo Chequing account makes shared spending simpler.

The complete guide to joint accounts in Canada

What is a joint bank account? Learn how joint accounts work in Canada, who can open one, the pros and cons, and how to pick the right account.

These credit cards earn the most cashback on gas in Canada

Compare the best gas credit cards in Canada by cashback rate, annual fee, and perks. See which card gives you the highest return at the pump in 2026.