Published on March 27, 2026 · 4 min read

By Julien Brault, founder of MooseMoney.

Building credit at 18 starts with getting your first credit card (step 1), migrating to a phone plan under your name (step 2), making payment on time (step 3) and motoring your credit score (step 4). Those steps are important because your credit score will influence your ability to rent an apartment, get a car loan, land certain jobs, and qualify for competitive interest rates for decades to come. The earlier you begin, the longer your credit history grows and the stronger your financial profile becomes.

"When you turn 18, if you're a student, you might be able to get an unsecured student credit card; if not, getting a secured credit card is a great way to build your credit too," stated Richard Goyder, Chief Credit Risk Officer at Neo Financial.

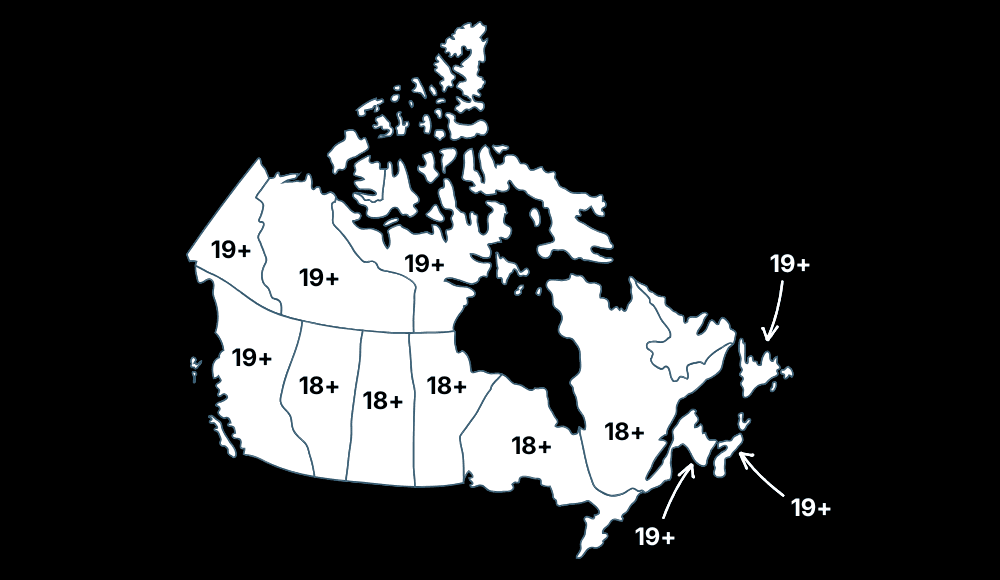

One important note for anyone under 18 who is reading this and planning ahead: you cannot get a credit card on your own until you reach the age of majority in your province or territory, which is either 18 or 19 depending on your province of residence. Julie Kuzmic, Head of Consumer Advocacy and Compliance at Equifax Canada, confirmed this directly: "Creditors generally won't give an account directly to an individual who is below the age of majority in their province."

You should be cautious about following credit building tips from Americans on TikTok or the web, since credit scores are not calculated the same way in Canada. Kuzmic give an example: "In the US, a common advice is that parents should get a secondary credit card for their child as they're getting older in order to build their credit history. Unfortunately, this does not work in Canada, as Canadian credit card issuers that offer secondary cards rarely report the activity on that secondary card to the second person's credit bureau."

Step 1: Get Your First Credit Card

Your first decision is choosing between a secured credit card and a student credit card. A secured credit card like the Secured Neo Mastercard requires you to provide a refundable cash deposit, and that deposit typically becomes your credit limit. If you deposit $300, your limit is $300. The card issuer assumes almost no risk, so approval is straightforward even with no credit history at all. Your payment activity gets reported to Equifax and TransUnion, which builds your credit file over time and, in the case of the Secured Neo card, you even earn cash back on your spending.

A student credit card is an unsecured option available through many banks and is designed for post-secondary students. These cards generally come with low credit limits, no annual fee, and usually does not offer any cash back. If you qualify for a student card, it functions the same way as any other credit card for credit-building purposes, and you avoid tying up cash in a deposit.

Step 2: Migrate to a Cell Phone Plan Under Your Own Name

Staying on your parents' mobile family plan is obviously cheaper, but it does absolutely nothing for your credit score because the account isn't in your name. If you want to actually start building a history, you need to migrate to a post-paid (monthly) plan under your own name. It turns a bill you’re already paying into a "trade line" on your credit report, proving to lenders that you can handle a recurring monthly commitment without flaking.

Step 3: Build the Habits That Raise Your Score

Pay your full statement balance every month. If you cannot pay in full, you must at least make the minimum payment by the due date to avoid a late payment being reported to the credit bureaus. Setting up automatic payments through your chequing account is the simplest way to ensure you never miss a due date. Use your card for small, planned purchases you can afford, such as groceries or a streaming subscription, and then pay the bill immediately or when the statement arrives.

Keep your utilization low. On a $500 limit, that means spending no more than $150 before paying it off. If you find yourself regularly approaching your limit, you can make multiple payments within a billing cycle to bring your reported balance down.

Do not close your first credit card (especially if it's one with no annual fee), once you qualify for a better one later. The age of that account contributes to your credit history length, and closing it shortens your average account age.

Step 4: Monitor Your Credit Report for Errors

Once you have an active credit product, check your credit report at least once a year from both Equifax and TransUnion. Several free apps such as Borrowell, Credit Karma, ClearScore and Neo (through its Build membership) also provide credit score monitoring. Look for incorrect personal information, payments inaccurately marked as late, and accounts you did not open. If you spot an error, you can file a dispute directly with the credit bureaus to have it corrected. Inaccurate data left unchallenged can drag your score down for years.

It typically takes about three to six months of reported activity before Equifax generates your first credit score. From there, building a good to excellent score is a process that takes years of consistent, responsible use. There are no shortcuts, but every on-time payment moves you in the right direction.

Related Posts

View All

Does Getting Your Rent Payments Reported to Credit Bureaus Actually Help You Build Your Credit in Canada?

Over the last few years, various rent reporting services have emerged in Canada, most of which only report rent payments data to Equifax. That includes Borrowell Rent Advantage, FrontLobby, and KOHO. More recently, rent reporting company Zenbase anno

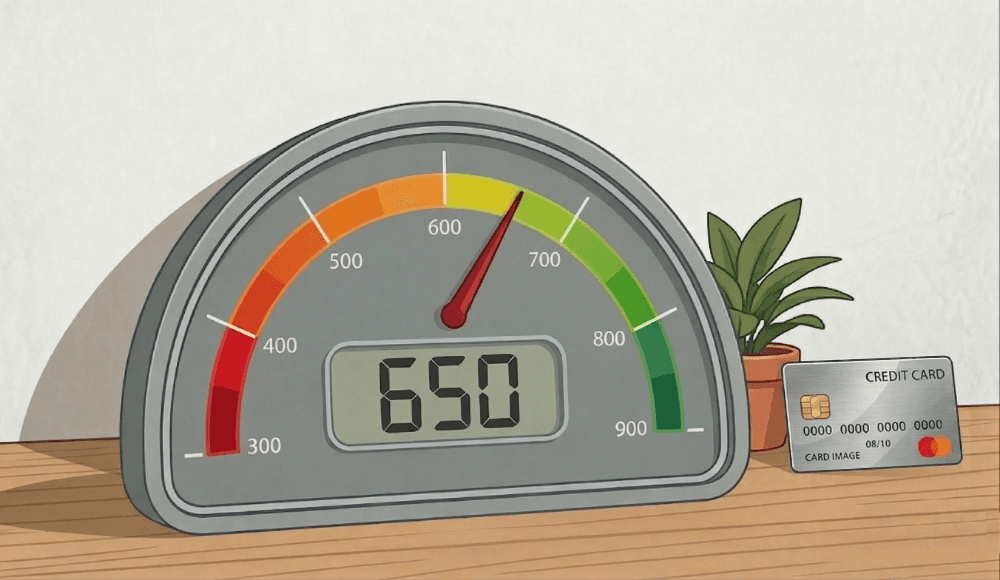

What You Can and Can't Do With a 650 Credit Score in Canada

You can still qualify for car loans, high interest personal loans, and secured credit cards, but you will face higher interest rates.

How to Freeze Your Credit and Avoid Credit Fraud in Canada

"If you're concerned about people opening up credit in your name or if your info were part of a leak, freezing your credit file is something you should consider."