Published on January 9, 2026 · 5 min read

For this week’s No More Ls column, we’re looking at how costly the fear of debt can be.

Millions of Canadians live with debt, but not everybody is comfortable with it. FP Canada’s 2025 Financial Stress Index survey found 52% of people agree that they are “afraid of making the wrong financial decision.” No surprise then that the difficult choices and hard truths which come with setting up a debt repayment strategy are enough to make some folks’ blood run cold. Trepidation toward your debts only makes things worse—the more you ignore debt, the bigger it can grow in the shadows.

Dealing with fear

Let’s address the dread of debt. Chantel Chapman, author of The Trauma of Money, says this type of thinking can hurt people. But she stops short of calling it fear. “I think they’re in a state of avoidance and vagueness,” she says. People who ignore debt know on some level that if they pay off what they owe, they’ll no longer feel the associated shame. That still doesn’t make it any easier to do, no matter how much you owe.

“It’s really hard to compare the amount of shame that someone carries based on the quantitative value of debt, because there are so many other aspects that go into the creation of that shame,” says Chapman. This includes your income bracket, where you live or were raised, or your experience with personal traumas and challenges. For newcomers to Canada, it might even be a misunderstanding of Canada’s financial culture. Debt is very common in daily life in Canada, from credit cards to car loans and mortgages.

But fear not. Mental and tactical strategies exist, says Chapman, which can help empower you to tackle debt fearlessly, one step at a time.

What causes debt shame

First things first: If you’re uncomfortable dealing with debt, ask yourself why that is. For many, this requires acknowledging feelings of debt-related shame.

“That’s so powerful as a first step,” Chapman says. Figuring out “the why” is empowering. Otherwise, people “don't want to interact with debt, because the moment they start moving toward paying it off, it’s in their face. They’re confronted with the cause of their shame.”

She says debt-related shame can lead people to two key behaviours that compound their problems and stoke fearful feelings.

One way people respond is avoiding debt, like ignoring monthly statements or neglecting to create a payment plan.

“The thing about avoidance is that the suffering doesn’t completely go away,” she says. “It just sits in the back of your mind like a tab open on your computer screen, slowing your whole operating system down.” And that can cause future problems, like growing debt, a hit to your credit score, higher interest rates and more. That’s not to be feared, but to acknowledge that today’s actions have later consequences.

Another possible response is “compulsive, soothing behaviours,” Chapman says, like spending money impulsively to make yourself feel better. Though this may help you feel better briefly, it can also create more of the debt that’s worrying you already.

Remove the feeling of shame by understanding you’re not alone

Shame comes from feeling alone and insecure with your struggles. And the private, personal journey of tackling debt can be isolating, but Chapman says “trying to seek a sense of belonging in the experience” is the best antidote. “You start to depersonalize the burden of responsibility by acknowledging this is actually a societal thing that I'm interacting with. This is a systemic thing.”

Make no mistake, this doesn’t mean you can forget your own role in creating the debt (you spent the money, after all), but it’s important to understand how accruing debt plays into something larger than yourself.

We live in a society where most people take on debt at some point—to purchase homes, seek higher education or even supplement paycheques in lean times. In the third quarter of 2025, total consumer debt in Canada was a whopping $2.6 trillion, according to the credit bureau TransUnion, so debt is definitely not just a you problem.

When you understand that the experience of owing money is shared by many others, “the need to avoid or soothe yourself is not as strong because you feel a sense of belonging.” Chapman says.

How to get comfortable with debt

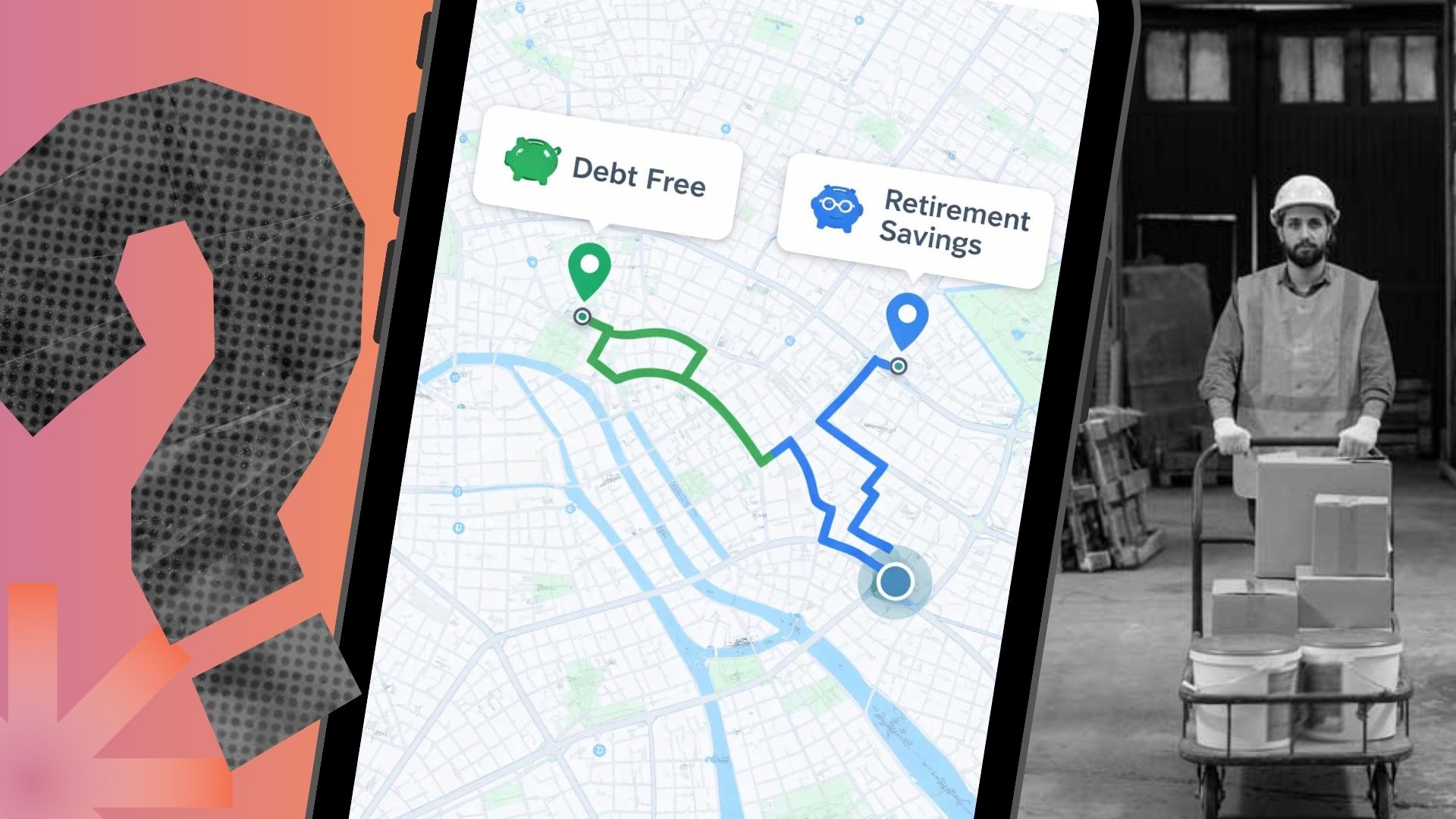

You can reframe the heavy feelings of debt by thinking of it as credit, which is a tool. Chapman also recommends that instead of looking at debt as a big mountain to scale in one go, it’s helpful to identify milestones and celebrate your progress along the journey to your ultimate goal.

“One thing I recommend is easing yourself into something that feels accessible without creating a ton of restrictions, so you don’t go into feast-and-famine cycles,” she says. This could include using a secured credit card (in which you control your credit, limiting it to the amount you put on the card), starting with a moderate debt repayment budget until you get used to it, or cutting some low-hanging fruit, as in variable expenses like dining out or subscription services.

As for celebrating credit wins, Chapman says, the first milestone with credit card or line of credit debt might be to pay it down to a certain utilization level (the percentage of available credit that you’re currently using). You might even choose to commemorate increases in your credit score (some banking apps offer tracking for clients). For those unsure where to start, even researching debt payback plans might be a first step worth celebrating. (Check out these 10 AI prompts that will save you money.)

“Every time you celebrate mini-milestones, you’re essentially working with your dopamine system, which motivates you to hit the next milestone,” Chapman says. And that is better than any retail therapy purchase. With the right attitude and a realistic plan, you can work toward a lower-debt lifestyle, and find reasons to celebrate along the way.

By Rob Csernyik

Rob Csernyik is an award-winning, full-time freelance journalist specializing in business and investigative reporting, as well as long-form features.

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.