Published on March 27, 2026 · 4 min read

By Julien Brault, founder of MooseMoney.

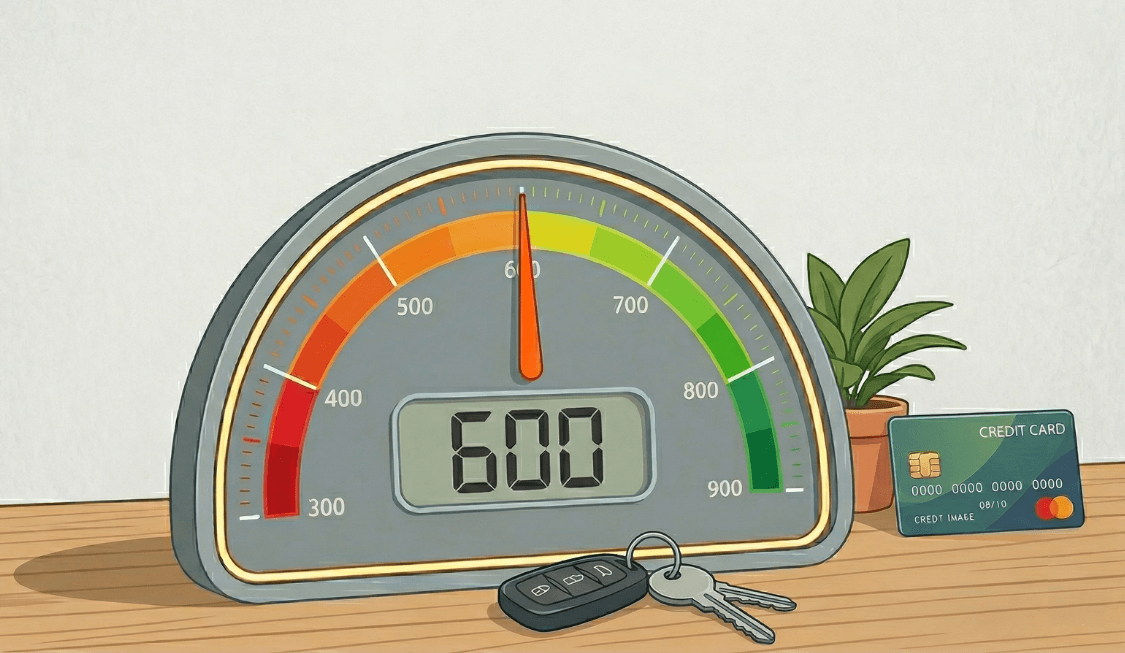

A 600 credit score in Canada can be limiting, but the good news is that you still have access to some credit products. "With a 600 credit score, you're definitely subprime; you can have access to some credit, but it will be at a very high interest rate and only subprime lenders will be prepared to lend you money at a very high interest rate," said Richard Goyder, Chief Credit Risk Officer at Neo Financial.

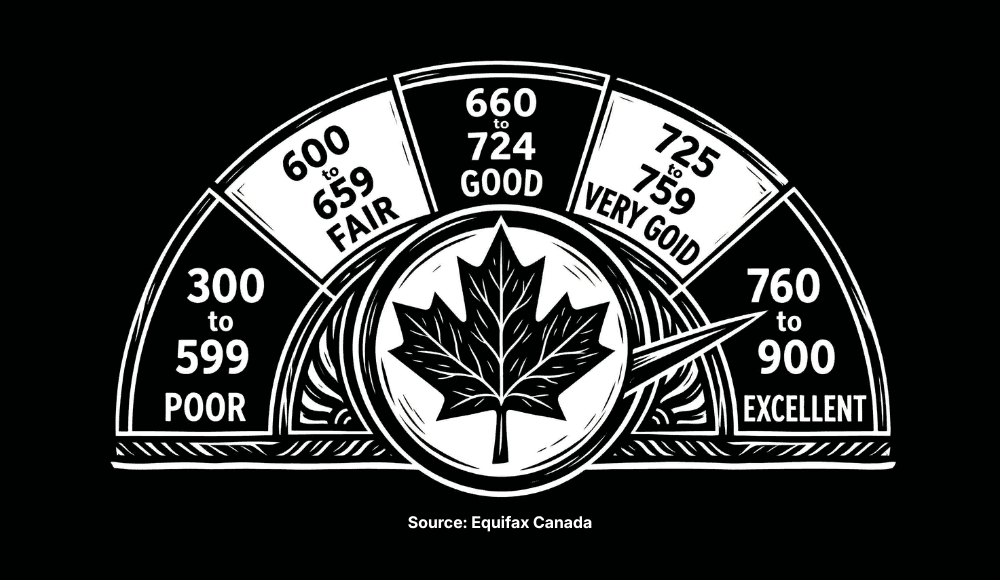

According to Equifax Canada, a 600 credit score is considered fair, since it falls on the low end of the 600 to 659 range. Anything below 600 is considered poor, so while a 600 credit score might be “fair” based on this scale, it is not a great credit score, and is also well below the Canadian average, which hovers around 660.

One thing worth knowing is that there is no universal, standardized label attached to your score when a lender pulls your file. Julie Kuzmic, Head of Consumer Advocacy and Compliance at Equifax Canada, clarified this point directly. "When the lender sends a request for somebody's credit file, what is sent back to them is the credit file and the score. There is not a label that gets sent like fair or good. That's entirely up to the lender to interpret the report," said Kuzmic. Each lender sets its own thresholds, which means a score of 600 might get you approved at one institution and declined at another.

What a 600 Score Qualifies You For

You can still get approved for certain credit products at 600, but the terms will reflect the risk lenders see in your profile. Personal loans from alternative or subprime lenders may be available, though you should expect interest rates significantly higher than what borrowers with good credit receive. Canada's major banks generally require a minimum score around 650 or higher for their unsecured personal loan products.

Credit cards become more accessible through secured options. A secured credit card requires you to provide a cash deposit that typically equals your credit limit, which reduces the lender's risk. The Secured Neo Mastercard, for example, is one product designed for Canadians who are building or rebuilding credit, and it reports your payment activity to the credit bureaus. Making on-time payments on a secured card builds a positive history on your credit report over time.

Standard unsecured credit cards with low credit limits may also be available through some issuers, but you will not qualify for premium rewards cards, travel cards, or cards with high limits. Car loans are possible at 600, though some dealerships and lenders require a minimum of 630. You can improve your approval odds by offering a larger down payment or bringing a co-signer.

Mortgages are the hardest product to access at this score. Most traditional mortgage lenders in Canada require a minimum score of 680. Some alternative mortgage lenders will work with borrowers between 600 and 680, but they charge higher interest rates and may require larger down payments. The cost difference over a 25-year amortization can amount to tens of thousands of dollars.

A 600 score can also affect non-lending areas of your life. Some landlords check credit before approving rental applications, and certain employers in financial services run credit checks as part of their hiring process.

How to Move Your Score Higher

Richard Goyder from Neo Financial is direct about what a 600 score demands. "If your score is 600, then, you definitely want to be taking steps to rebuild your credit score," he explained.

Paying every bill on time is the single most effective thing you can do. A single missed payment can drop your score by as much as 150 points, and negative payment information stays on your credit report for six to seven years in most provinces. You should set up automatic payments or calendar reminders for every account you hold, including credit cards, phone bills, and any loans.

Keeping your credit utilization below 30% of your total available credit is the second priority. If your credit card limit is $1,000, you should aim to keep your balance below $300 at all times. You can also ask your card issuer for a credit limit increase, which lowers your utilization ratio as long as your spending stays the same.

Pulling your own credit report from Equifax or TransUnion counts as a soft inquiry and will not hurt your score. You should review your report at least once a year to check for errors or signs of fraud, and dispute any inaccuracies directly with the bureau. Incorrect information on your report could be dragging your score down without your knowledge.

A secured credit card like the Secured Neo Mastercard can help you establish a consistent record of on-time payments if your current credit file is thin or damaged. These products are specifically designed to report positive payment behaviour to the bureaus, which gradually rebuilds your score over months and years.

Related Posts

View All

Does Getting Your Rent Payments Reported to Credit Bureaus Actually Help You Build Your Credit in Canada?

Over the last few years, various rent reporting services have emerged in Canada, most of which only report rent payments data to Equifax. That includes Borrowell Rent Advantage, FrontLobby, and KOHO. More recently, rent reporting company Zenbase anno

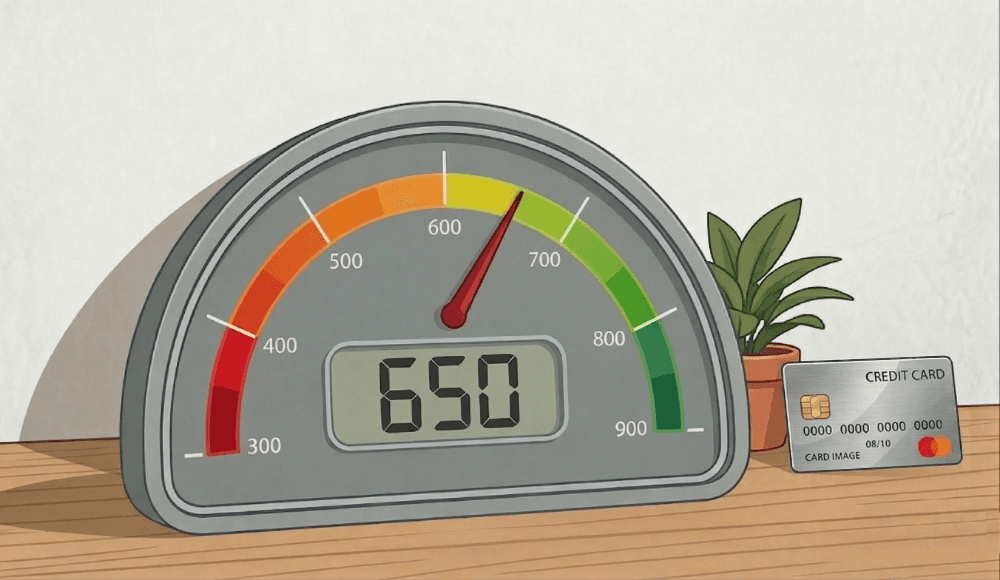

What You Can and Can't Do With a 650 Credit Score in Canada

You can still qualify for car loans, high interest personal loans, and secured credit cards, but you will face higher interest rates.

How to Freeze Your Credit and Avoid Credit Fraud in Canada

"If you're concerned about people opening up credit in your name or if your info were part of a leak, freezing your credit file is something you should consider."