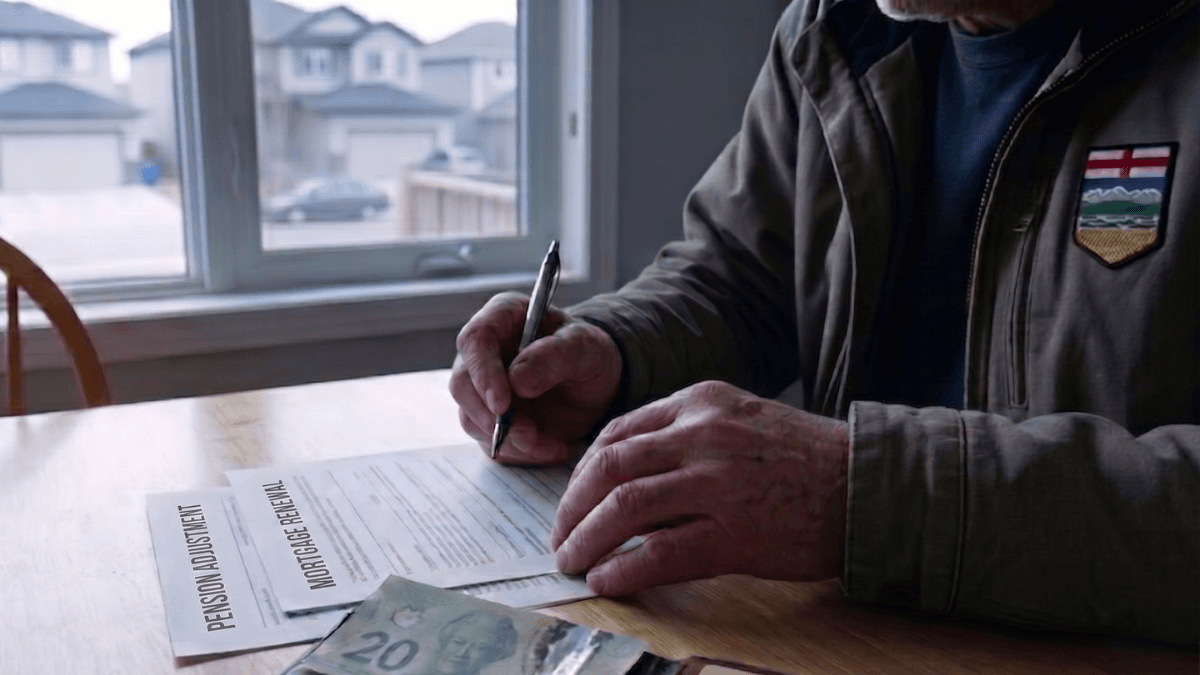

Of course you have questions about Alberta separating from Canada. What does it mean? How will it happen? But there are questions that are even closer to home: How will it affect your finances? Every Albertan with savings accounts, registered accounts, a pension and a mortgage could be affected by this possible referendum. Plus, it may also affect taxes and affordability. Here are the questions we should be asking of the debate.

How can the Alberta Separation affect your savings protection?

Know that your deposits today are almost certainly covered. But let’s look at what could happen to the insurance coverage on your accounts. The Canada Deposit Insurance Corporation (CDIC) is a federal organization that protects eligible deposits up to $100,000 per category at member institutions. If Alberta were to separate, that means it would need to build its own equivalent from the ground up, or negotiate a continued membership with the CDIC, or operate without this coverage during however long the transition could take. The first option would take time and the last one isn’t ideal. But a transition agreement makes sense for all parties involved, as it would protect everyone, including the banks.

You pay into the Canadian Pension Plan (CPP), so would you still qualify for it?

You may have heard of the Alberta Pension Plan (APP) before. And that’s because the provincial government commissioned a report in 2023 about creating its own pension plan. It projected Albertans’ share of the Canadian Pension Plan (CPP) to be about $334 billion, which is more than half of the total CPP assets.

Money is tough conversation after any breakup, let alone one of this size. And right now, the contested amount of the APP’s share is still being debated.

Quebec has its own pension plan, but the path for Alberta would be different. The Québec Pension Plan (QPP) was created because Quebec opted out of CPP in the beginning. If Alberta wants to leave, it needs to give CPP three years’ notice.

What’s the impact on your mortgage or ability to buy a property?

So, what does the breaking away from Canada mean if you’re planning to buy within the next five to 10 years? Lots.

Canada’s banking system allows for you to get the best rate and best mortgage from a lender in Canada, even if it’s outside your province. That includes federally regulated institutions, who are licensed to lend in Alberta.

But if you have mortgage default insurance because you didn’t have the ability to put down 20% of the home’s value as a downpayment, you’ll want to find out what that means for your loan. The Canada Mortgage and Housing Corporation (CMHC) provides this insurance, which is, of course, a federal program. Should the referendum vote lean to a divide, it would raise questions for CHMC-covered properties in Alberta.

Then there are the lending rules by the Office of the Superintendent of Financial Institutions (OSFI). Known as the OSFI B-20 rule, these regulations include the Stress Test, a calculation on your ability to make payments should rates, the economy or your financial situation change, as well as income verification, and loan to value limits. So, Alberta would need to build its own regulations.

What would happen to your registered accounts?

Alberta claiming independence from Canada requires looking at the tax rules whether or not you hold cash or investments inside a registered account. Things like contribution room, deduction limits and new accounts for registered accounts, like TFSAs, RRSPs, FHSAs and more, are all created by federal legislation and administered by the Canada Revenue Agency (CRA) under the Income Tax Act. And that would need to be recreated under an independent Alberta, as none of this has been worked out yet.

And if you own foreign investments, you already know how withholding tax affects your portfolio. Canadian investments outside of Alberta may also require similar treatment, too.

Could your paycheque benefit?

Of course, Alberta has a progressive income tax system with a provincial income tax rates ladder. It’s levied under the Alberta Personal Income Tax Act and collected by the CRA for the province. Employment Insurance (EI) premiums collected and managed federally. While Albertans currently pay both federal and provincial income tax, plus GST on goods and services, it doesn’t have a provincial sales tax.

Under separation, the federal layer goes away. That may mean no federal income tax, no EI or CPP premiums and no GST.

At first read, this sounds like a financial windfall. But Alberta would need to replace that revenue through its own fiscal framework, especially for EI.

How, and at what rates, are questions the province has yet to answer publicly.

What a separation realistically means for Albertans’ finances

A negotiated separation with transition arrangements is a realistic scenario. But these are the questions that need to be seriously asked. The referendum debate is happening. The financial questions are real. The best thing Albertans can do right now is ask for answers to the questions above. Get answers about what will happen to CPP, CDIC insurance, taxes on registered accounts, and more. This is one of the biggest decisions in the province's history, and no one can afford to be complacent.

The political case for or against separation is something Albertans are debating. There is a clear financial case for getting specific answers before a vote is cast. That part seems pretty clear.

Neo Financial serves over one million Canadians, including hundreds of thousands of Albertans.

---

Disclaimer: This article provides information and is not intended to provide any personalized tax, investment, financial, or legal advice. You are encouraged to seek professional advice before making financial decisions.

Related Posts

View All

Strengthening our senior leadership team at Neo Financial

We are thrilled to share the appointment of several new senior leaders at Neo. Please join us in welcoming Amanda Broos as Chief People Officer, Dana Saric as Chief Legal Officer, Allemander Neto as Acting Chief Financial Officer, James Nauss as Chief Operating Officer, and Stefan Doan as Chief Information Officer.

2024 recap

A review of the event-filled year and a look forward to 2025.

Neo Financial adds new senior leaders from Nubank, Tangerine, and Rappi

We're excited to announce the addition of Tim Morris as Chief Banking Officer, Rafael Mejia as Chief Growth Officer, and William Tsutsumida as Chief Credit Risk Officer to the Neo Financial team to support Neo's mission to transform Canada's financial service experience by creating the most rewarding experience in Canada.