By Julien Brault, founder of MooseMoney.

Opening a savings account for your child is one of the simplest ways to teach them about money before they need to manage it on their own. The best youth bank account in Canada charge no monthly fees, pay a competitive interest rate, and give your child access to app-based banking so they can watch their balance grow. Below are three accounts worth comparing in 2026.

While some digital banks require a parent's consent for younger teens, many traditional banks in Canada allow youths to open an account without parents' permission as early as age 13 or 14. Most banks require a birth certificate for younger children and a secondary piece of ID plus a Social Insurance Number (SIN) for older teens. Knowing what paperwork you need before you start will save a trip.

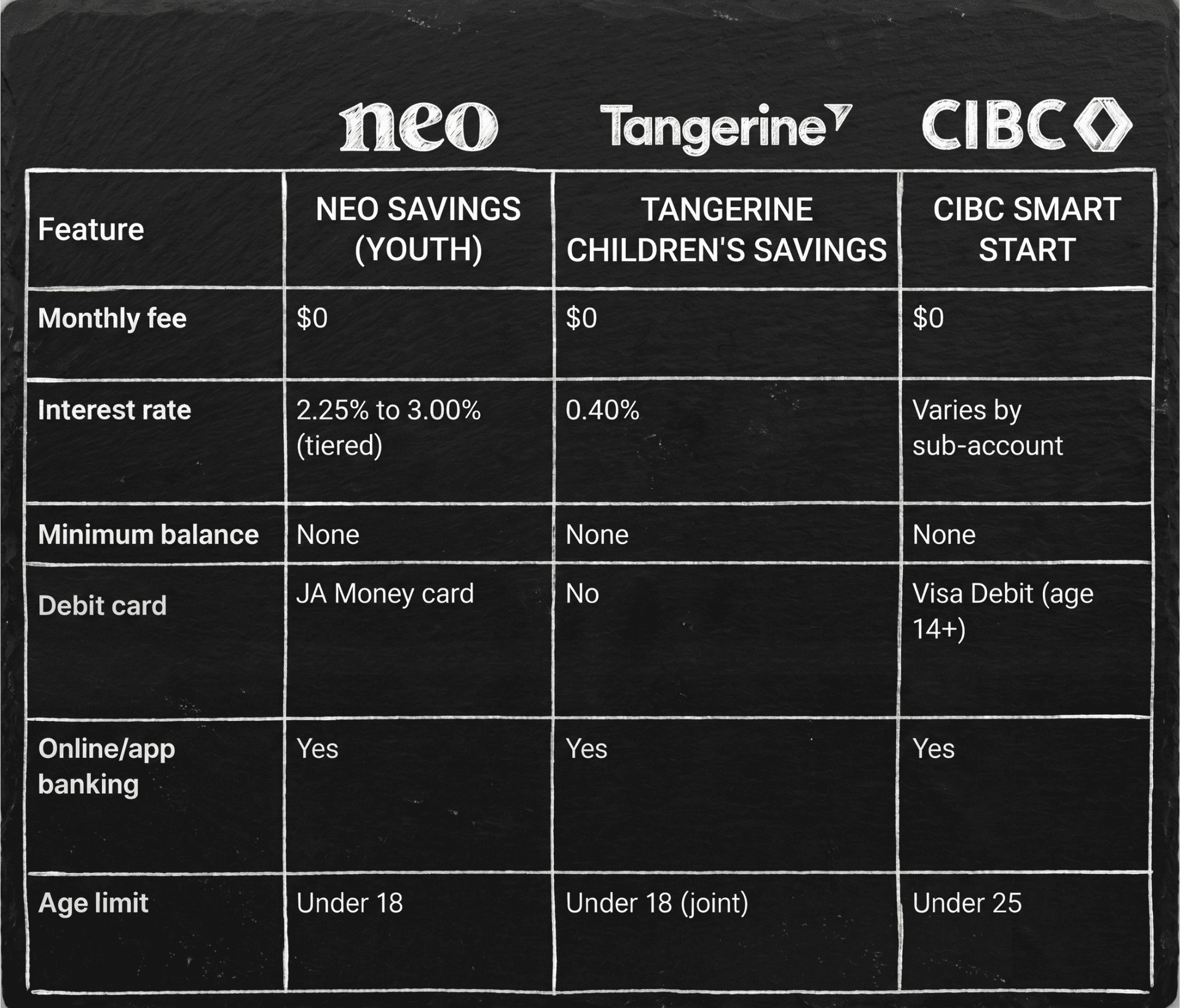

1. Neo Savings Account for Youth

Neo Savings Account for Youth is available to Canadians between 13 and 18 (14 to 18 in Quebec) and can be opened through the Neo Financial app with a parent or guardian's consent. It pays a tiered interest rate, and this is where you need to read the fine print. While it advertises up to 3.00%, that top tier only applies to balances of $20,000 or more. For more realistic youth savings, the account pays 2.25% on balances up to $4,999.99, and 2.50% on balances between $5,000 and $19,999.99. Despite the tiered structure, there are no monthly fees, no minimum balance requirements, and no temporary promotional rates that drop after a few months, making it easy to predict how much your child's savings will earn. The account is managed entirely through the Neo app, and parents maintain oversight while their child learns to navigate digital banking.

2. Tangerine Children's Savings Account

Tangerine Children's Savings Account is structured as a joint account between a parent and child, but the child receives their own client number and login credentials. This setup lets kids track their balance independently while a parent retains full access. The account charges no monthly fees and has no minimum balance requirement. It currently pays 0.40% interest. Because Tangerine operates without physical branches, like Neo Financial does, all account management happens online or by phone, so the parent must already be a Tangerine client to open one. The lower interest rate is a trade-off, but the independent login feature is a useful tool for teaching kids to monitor their own finances.

3. CIBC Smart Start Account

CIBC Smart Start Account is available to Canadian residents under 25 and charges no monthly fees. For children under 14, a parent opens and manages the account, with the option to set up recurring transfers for allowance payments. Once the child turns 14, they can open or manage an account independently (with or without parental signing authority), gain access to their own app, unlimited transactions, unlimited Interac e-Transfers, and a Visa Debit card for online purchases. CIBC also offers the CIBC eAdvantage Savings Account where youth can earn interest on saved funds. The account's longevity is a strong advantage because your child can keep it fee-free through university without needing to switch banks.

Neo Savings Account for Youth Vs. Tangerine Children's Savings Account Vs CIBC Smart Start Account

How We Picked These Three Accounts

We evaluated youth savings accounts on monthly fees, interest rates, transaction limits, debit card availability, and the quality of the digital banking experience. We also considered whether the account can grow with the child into their late teens or early twenties. Full disclosure: Neo Financial is the publisher of this content, so we are biased toward listing the Neo Savings account, but we still believe it earns a spot on merit, and we encourage you to compare all three before deciding.

Do Kids Need To Pay Taxes On Interests?

Parents sometimes wonder whether a youth savings account will create a tax headache. “Very few kids will owe income tax on their savings account interest, since the basic personal amount they can earn tax-free is $16,452, but everyone's personal situation is unique and you should always seek assistance with any individual tax questions,” said Tim Morris, Chief Banking Officer at Neo Financial. A child would need to earn above that threshold before any tax applied to their interest earnings, so for the vast majority of families, this is a non-issue. One detail worth noting is that interest earned in a joint account where the parent deposited the money may be attributed back to the parent for tax purposes under Canada's income attribution rules.

Related Posts

View All

Here Are The Top 3 No-Fee Joint Bank Accounts in Canada

We picked the following three joint accounts because they charge no monthly fees, require no minimum balance to avoid fees and benefit from CDIC coverage:

The 4 High Interest Savings Accounts (HISA) ETFs Every Canadian Should Know About

Canadian investors looking for a low-risk place to park cash inside a brokerage account should consider those four HISA ETFs in 2026. These funds hold deposits at Canadian banks, earn interest on those deposits, and pass the income to unitholders.

Bank account types: What’s the best bank account?

Which bank account is best for you? To decide that, we want to look at interest, flexibility and fees.