Published on March 2, 2026 · 5 min read

Here’s the answer to this week’s reader question.

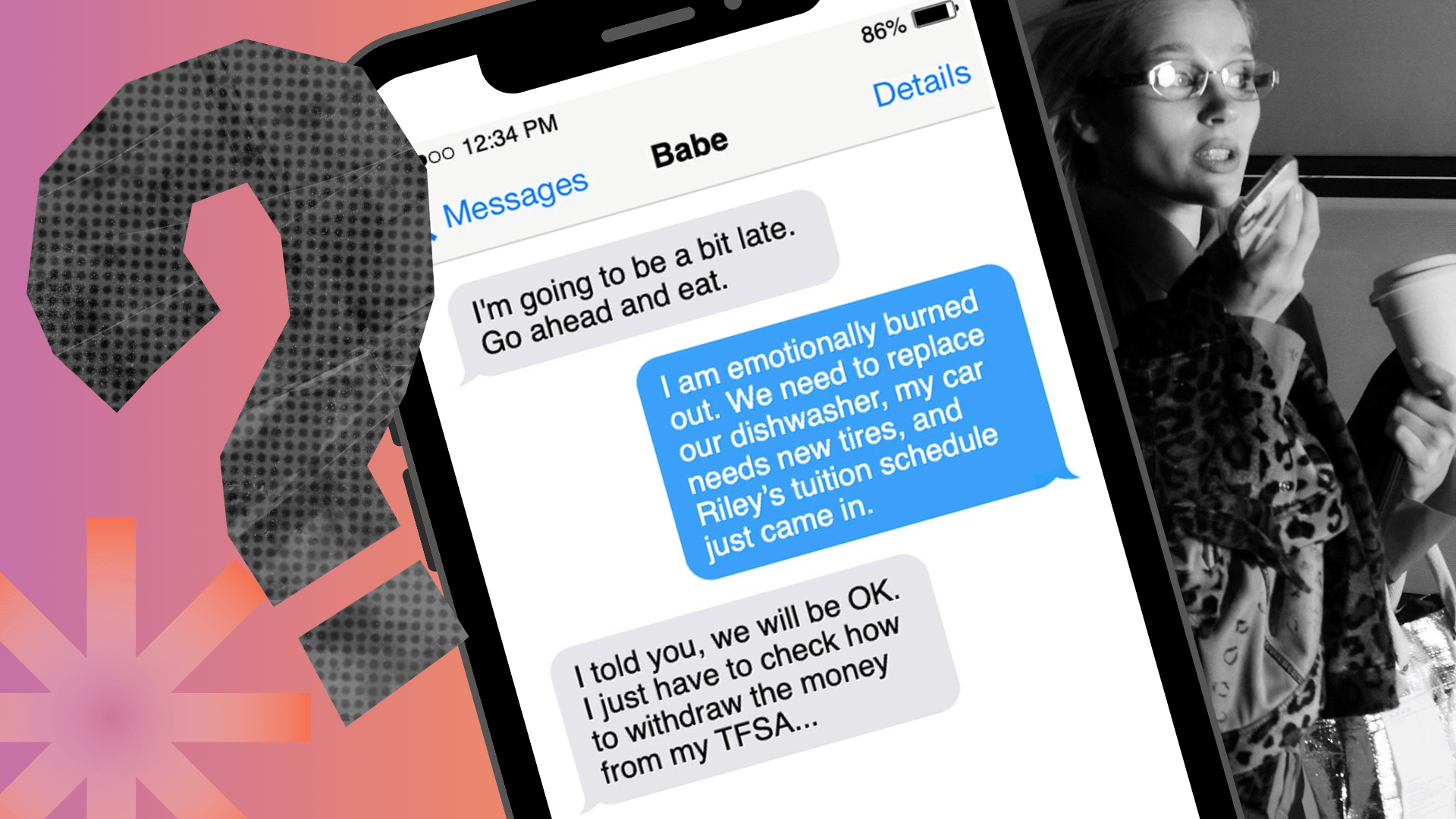

“Most of my savings are in registered savings plans. How can I access that money in an emergency?”—Henry

From our sponsor

-YS2E1V5zsVvJnoAtXQiL0jjcELgptM.png&w=1920&q=75)

By Anita Bruinsma, CFP, CFA, Clarity Personal Finance in Toronto

As told to Ian Portsmouth

If you need cash fast and you don’t have an emergency savings fund, you may be tempted to withdraw funds from any registered accounts you have, such as a registered retirement savings plan (RRSP). That’s one of seven registered accounts Canadians have access to:

- RRSP

- Tax-free savings account (TFSA)

- First home savings account (FHSA)

- Registered disability savings plan (RDSP)

- Registered education savings plan (RESP)

- Registered retirement income fund (RRIF)

- Locked-in account (LIRA/LIF)

Of those seven types of registered accounts recognized by the government, the first five listed are familiar to many Canadians and offer a reasonably short withdrawal timeline. But the amount of money that ends up in your pocket and your ability to achieve long-term financial goals depends on which type of registered account you draw from.

Withdrawing from an RRSP for an emergency

There are a few drawbacks to taking the money out of an RRSP. The withdrawal is taxed as regular income and you’ll pay a withholding tax ranging from 10% for amounts under $5,000 (5% in Quebec) to 30% for amounts over $15,000. And once you take money out of an RRSP, you never get that contribution room back, unlike with a TFSA. That’s not a huge concern for people who have a lot of RRSP contribution room. But withdrawing from your RRSP negates a lot of that hard work you did planning for your retirement, investing your money and letting it grow. So, an RRSP is probably the last place I would take emergency funds from.

Withdrawing from a TFSA for an emergency

Generally, the first place to look for emergency funds is your TFSA, because it’s the most flexible of all the registered account types. When you take money out of a TFSA, you don’t lose any contribution room if you replace that amount by the end of the next year. Also, your withdrawals aren’t taxable because any investment growth within a TFSA is considered tax-free income, and your original contributions to a TFSA were made with after-tax dollars.

That’s different from the tax-deductible dollars you contribute to your RRSP, which is a tax-deferral tool, meaning you pay tax when you withdraw, not when you deposit the money. Your next best option depends on your situation.

Withdrawing from an FHSA for an emergency

If you take money out of your FHSA, you’ll compromise your ability to save for a down payment on your first home—but addressing your financial emergency may be more urgent. Generally, any amount withdrawn from your FHSA that’s not used to buy a home will be taxed as regular income, which also means that your financial institution will apply a withholding tax of up to 34% (paid directly to the government), depending on how much you withdraw and the province you live in (Quebec adds on a provincial withholding amount). If you live outside Quebec and withdraw $10,000 from your FHSA, for example, you’ll receive $8,000 and $2,000 will be held back for you to apply toward your income taxes for the year.

Withdrawing from an RESP for an emergency

Taking emergency funds from an RESP could be suitable if you believe you’ve already saved enough, your kids can kick in with student loans or their own employment income, or they’re unlikely to pursue post-secondary education. But there’s a price to pay if you withdraw from your RESP for reasons other than paying for a child’s education. The contributions you made to the RESP won’t be taxed when they’re withdrawn, because they were made using after-tax dollars, as with a TFSA—but you will have to repay any government grants and bonds associated with those contributions. As for the investment earnings within the RESP, they will be taxed at your regular income tax level plus 20% (12% in Quebec). Speak to your RESP provider about other conditions and restrictions that apply to withdrawals.

Withdrawing from an RRIF for an emergency

If you’re already retired, you may have an RRIF. Any withdrawals from an RRIF are taxed as regular income (not capital gains) and, in fact, you’re required by law to withdraw a minimum amount per year. The only drawback is that the withdrawals could push your annual income over the threshold at which the government begins to claw back some of your Old Age Security benefits, starting in the following tax year.

How fast can you get the money from a registered account?

Some account types require more paperwork and processing time than others. Making a non-educational withdrawal from an RESP, for instance, could take a week or more. The types of holdings within an account and where they are held can also influence your withdrawal timeline. For instance, you can typically transfer cash immediately from a simple RRSP savings account into your chequing or savings account. But if the money is tied up in an investment vehicle, such as individual stocks or mutual funds, it could take two or three business days to sell those investments and have the funds transferred to your bank account.

When an urgent and unexpected financial need arises, having a sufficient emergency fund will help you protect your registered accounts. That’s why it’s one of the first things I discuss with clients before setting up a savings plan for retirement, a first home, or anything else. The optimal amount to save for an emergency depends on your individual situation, including the cost of supporting any dependents, whether you own a car or a home, and how quickly you can find new employment if you lose your job. It could be $5,000 or $30,000, but a common rule of thumb is enough to cover your essential living expenses for at least three months. And if you have a lot of TFSA contribution room, it makes sense to keep your emergency fund in a TFSA—provided it’s held in cash or investments that can be sold quickly. You want the money to be there when you need it.

The Get is owned by Neo Financial Technologies Inc. and the content it produces is for informational purposes only. Any views and opinions expressed are those of the individual authors or The Get editorial team and do not necessarily reflect the official policy or position of Neo Financial Technologies Inc. or any of its partners or affiliates.

Nothing in this newsletter is intended to constitute professional financial, legal, or tax advice, and should not be the sole source for making any financial decisions. Past performance is not a guarantee of future results. Neo Financial Technologies Inc. does not endorse any third-party views referenced in this content. Always do your due diligence before deciding what to do with your money.

© 2026 Neo Financial Technologies Inc. All rights reserved.