Updated on June 17, 2026 · Published on June 12, 2026 · 7 min read

Published on June 15, 2026

A joint bank account lets two or more people deposit, withdraw and manage money from a shared account. Whether you’re merging household finances with a partner or pooling funds with a roommate to cover rent, opening a shared account is a practical way to streamline your monthly bills and build financial transparency together.

From our sponsor

-YS2E1V5zsVvJnoAtXQiL0jjcELgptM.png&w=1920&q=75)

This guide breaks down exactly how joint accounts work in Canada, who can open them, and how to choose a modern financial setup that keeps your money moving.

Key takeaways:

- A joint bank account gives two or more people equal access to shared funds.

- Any Canadian adult can open one—not just married couples.

- Joint accounts are eligible for separate Canada Deposit Insurance Corporation (CDIC) coverage, up to $100,000 per unique set of joint depositors.

- Interest must be reported to the Canada Revenue Agency (CRA) by contribution ratio (how much each deposits). It’s not split 50/50.

- Right of survivorship means funds pass directly to the surviving holder.

What is a joint bank account?

A joint bank account is a financial account owned equally by two or more people, where each person can deposit, withdraw and manage the funds. Because there is no single owner, any account holder can make day-to-day transactions, pay bills, and use linked debit or prepaid cards.

When you set up shared finances, you generally choose between two primary operational types:

- “And” accounts require signatures and consent of all account holders for every withdrawal and transaction.

- “Or” accounts is the more common of the two types, and this shared account allows any user to deposit or withdraw funds without needing permission from the other.

Joint chequing vs. joint savings: What’s the difference?

Choosing a joint account doesn’t mean giving up your financial independence. Many Canadians prefer a multiple-account approach: maintaining individual personal savings or chequing accounts for private spending while utilizing a joint bank account specifically for collective expenses.

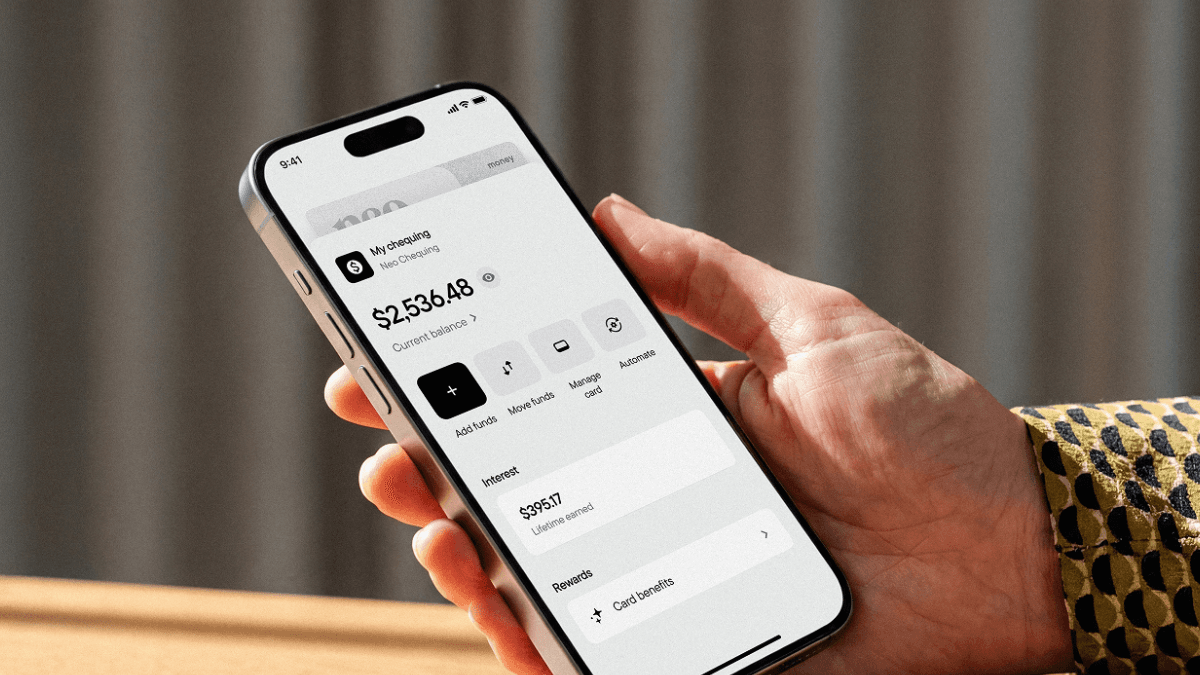

New from Neo: Skip the traditional branch lines and enjoy everyday shared spending. Introducing joint Neo Chequing—built to help you track household expenses in real time.

How joint bank accounts work in Canada

Having a joint account in Canada comes with unique rules regarding access, accountability and deposit protection.

First, both account holders get equal rights to funds, regardless of who originally earned or deposited the money.

Shared funds also come with shared liability. Account holders are equally responsible for all transactions. If the account is overdrawn or incurs a fee, the financial institution can collect the full amount from either party.

The CDIC insurance advantage

A significant financial benefit of shared accounts comes down to protection via the CDIC.

Eligible deposits held at a CDIC member institution are insured for up to $100,000 per account, per person. Deposits in a joint account fall under a completely separate category from your individual personal accounts, meaning your joint account category is insured up to an additional $100,000 per unique set of owners. This effectively doubles your overall deposit protection.

Joint account vs. authorized users vs. Power of Attorney

A joint account gives both parties complete ownership of the funds. If you want to collaborate on money management without giving away full legal ownership, there are alternatives like authorized users and Power of Attorney (POA).

Who can open a joint bank account in Canada?

The most common misconception about joint accounts is that they are reserved for married couples. In reality, any two (or more) Canadians who meet standard eligibility requirements (i.e. over the age of majority, have valid identification, etc.) can open an account together to simplify cash flow. Common shared financial setups include:

- Married and common-law couples, for managing shared mortgage payments, utilities, groceries childcare costs, and more.

- Unmarried partners, for navigating shared living expenses while maintaining individual financial autonomy.

- Roommates, for pooling funds seamlessly to cover rent, internet and household supplies.

- Parents and adult children, for assisting aging parents with bill payments, helping students manage living costs, and more.

- Small business partners, for co-owners managing shared corporate expenses—typically structured through specialized business or commercial accounts.

Legal and tax considerations for joint accounts in Canada

While a joint bank account makes daily spending simpler, the CRA views these accounts through a very specific legal lens.

Under Canadian tax law, interest earned in a joint account must be reported based on each person’s contribution ratio. It’s not automatically split 50/50. Misreporting this can trigger CRA attribution rules.

What happens if one person passes away?

In most Canadian provinces and territories, joint accounts are structured with the right of survivorship. Meaning, if one account holder dies, the ownership of the remaining funds automatically transfers directly to the surviving account holder. The money bypasses the deceased person’s estate entirely, meaning it is not subject to probate delays or estate administration fees, allowing the surviving partner to maintain continuous access to funds for immediate household needs.

A note for Quebec residents: Under Quebec civil law, a joint account is typically frozen upon the death of an account holder. Liquidators or surviving spouses can declare their respective shares to maintain access to a portion of the funds for immediate liquidation and funeral costs.

What happens to a joint account in a divorce or separation?

Because both parties have an equal legal right to the funds in a joint account, either person can legally withdraw the entire balance at any time.

During a separation or divorce, a joint account can become a significant point of friction. With Neo joint accounts, a single account holder can legally close the account on their own, meaning one person has the ability to withdraw the entire balance and shut the account down completely. If a relationship ends, the cleanest step may be for both parties to mutually agree to freeze or close the account and distribute the funds equitably.

Pros and cons of joint bank accounts

Still on the fence of whether to open a joint account or not with someone? We break down the benefits and potential pitfalls of opening a shared account below:

Pros of joint accounts

- Builds a clear, unified view of shared cash flow. For joint chequing accounts, this eliminates the need to manually Interac e-Transfer® money back and forth for shared bills. For joint savings, all account owners see how much money grows over time.

- Joint deposits qualify for a separate CDIC coverage category—up to an extra $100,000 per unique set of co-owners.

- Most joint accounts carry the right of survivorship, streamlining estate planning.

Cons of joint accounts

- Every transaction, purchase location, and amount is completely visible to all account holders, which can be a downside for people who want to keep their financial activity private.

- If one partner faces legal action, a tax judgment, or a debt collection order, the funds within the joint account can potentially be frozen or seized to satisfy that debt.

- In a separation, an uncooperative partner has the legal ability to clear out the account balance entirely.

How to choose a joint account

Traditional financial institutions often attach monthly maintenance fees or minimum balance requirements to shared accounts, which can quietly drain your collective progress. When comparing alternatives, prioritize digital-first platforms that remove these friction points. Keep an eye out for:

- Zero monthly fees to keep 100% of your money working toward your goals

- Real-time notifications to instantly update you on transactions

- Digital onboarding to allow you and your co-account owners to set up your account directly from your phones.

You can get started in minutes. Here’s how to open a joint bank account in Canada.

Frequently asked questions about joint accounts

Can I see what the other person spends on a joint account?

Yes, every transaction made by any account holder appears on the joint account statement. It typically shows the date, vendor and amount. If you prefer privacy for individual personal spending, consider maintaining an individual account separate from your shared one.

Can a joint bank account be opened online in Canada?

Yes. Modern financial platforms allow two or more people to link their profiles and complete identity verification online in minutes without needing to step into a physical location. Learn more about how to open a joint account online.

Can a creditor seize money from a joint account?

Yes. If one account holder owes money to a creditor or the CRA, the funds in the joint account may be subject to a garnishment order. All parties on the account are considered legal owners of the total balance.

Is a joint bank account right for me?

A joint account works best when both parties have mutual trust, aligned financial goals, and transparent spending habits. If you want shared bill management but want to keep your transactions private, consider a hybrid approach like keeping separate individual accounts alongside a joint account.

Do both people need to be present to open a joint bank account?

It used to be that way, when big banks were Canadians’ only options. But not anymore. Digital-first platforms like Neo allow both applicants to verify their identity and link their accounts online from separate locations.

How do I remove myself or someone else from a joint account?

In most cases, converting a joint account back into an individual account is not permitted. To remove a person, the existing shared account must be closed entirely.

What happens to a joint account if one person dies?

In most Canadian provinces, joint accounts include the right of survivorship. Funds automatically transfer to the surviving account holder, bypassing probate. Quebec is an exception: Accounts are typically frozen until the estate is settled.

By The Neo Editors

Neo’s editorial team does the heavy lifting—vetting the facts, stripping away the jargon, and breaking down complex mechanics—to bring you straightforward guides you can use to build credit and chart your financial journey.

Related Posts

View All

Should you open a joint chequing account? Here’s what you need to know

Learn how a joint chequing account works in Canada, who can open one, and how the joint Neo Chequing account makes shared spending simpler.

How to open a joint bank account in Canada

Opening a joint bank account in Canada is easier than most people think—but knowing what you're signing up for matters. Here's everything you need to know about opening a shared account.

4 no-fee Canadian bank accounts you should know about in 2026

If you are searching for the best no-fee bank account in Canada, these four options charge zero monthly fees while still offering competitive interest, unlimited transactions, and modern digital tools.