By Julien Brault, founder of MooseMoney.

If you owe more than you can repay, your two main options are a consumer proposal and personal bankruptcy. Both are governed by the Bankruptcy and Insolvency Act, both require a Licensed Insolvency Trustee (LIT), and both stop wage garnishments, collection calls, and interest charges the moment you file.

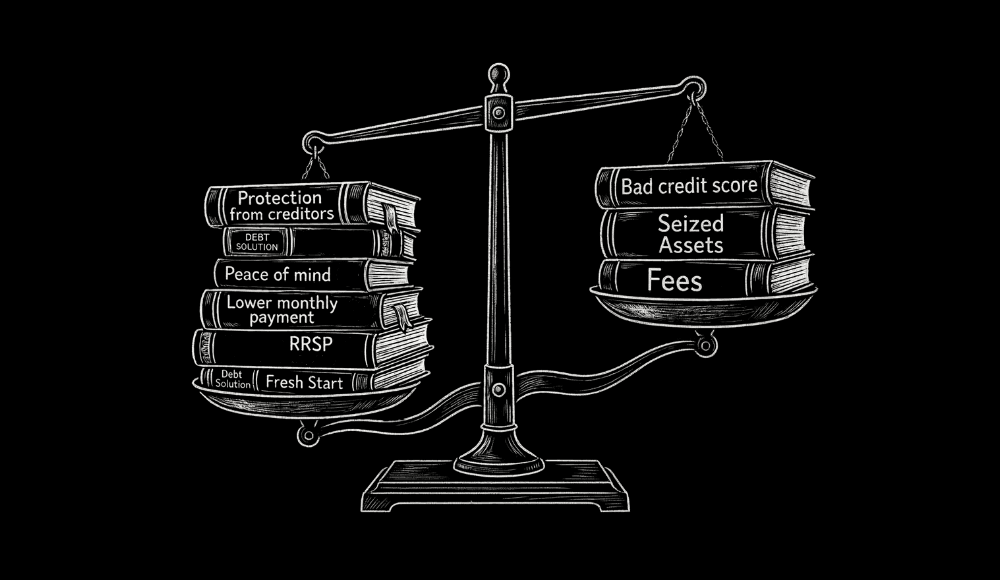

The critical difference is this: a consumer proposal lets you keep all your assets while repaying a negotiated portion of your debt over up to five years, whereas bankruptcy can eliminate your debts faster, but may require you, depending on your current assets and income, to surrender non-exempt assets and make surplus income payments. "Every debtor who can afford to make a viable proposal to their creditors should make an offer to settle before filing for bankruptcy," recommends Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.

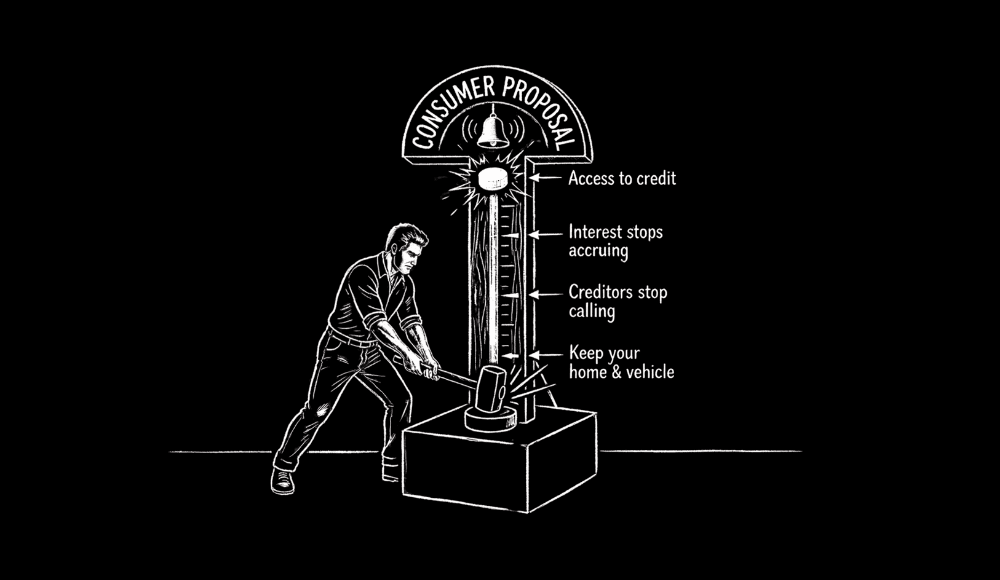

Here is what separates the two options in practical terms. A consumer proposal is available to anyone who owes less than $250,000 in unsecured debt (excluding a mortgage). You and your LIT negotiate a settlement with creditors, typically starting around 20 to 30 percent of your total unsecured debt, and you repay that amount through fixed monthly payments over up to five years. You can pay it off early without penalty. Your assets stay completely untouched. You receive an R7 credit rating, which remains on your credit report for three years after you complete the proposal or six years after filing, whichever comes first.

Bankruptcy, by contrast, requires a minimum of only $1,000 in debt, has no upper limit, and can discharge your obligations in as little as nine months for a first-time filing if you have no surplus income. If your income exceeds the government-set threshold, the process extends to 21 months, and you must make surplus income payments. A second bankruptcy lasts at least 24 months, or 36 months with surplus income.

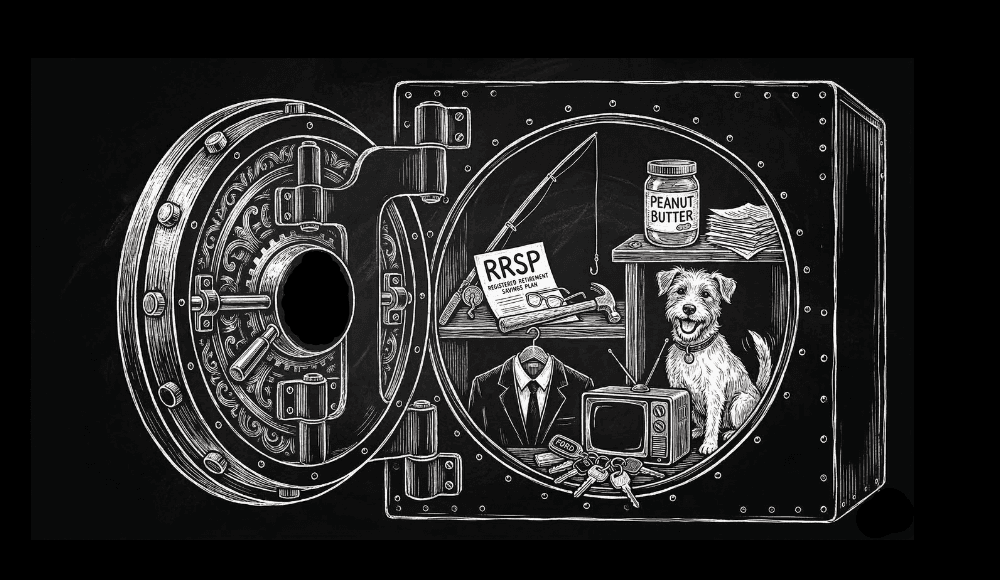

With a bankruptcy, you receive an R9 rating that stays on your credit report for six to seven years after your discharge. You must also surrender non-exempt assets, though provincial exemptions protect basic household items, clothing, tools of your trade and, in most provinces, a vehicle and a principal residence assuming your equity in those is not higher than what is permitted in each province.

Both processes require you to attend two mandatory credit counselling sessions and to fully disclose your assets and debts. Both cover most unsecured debts, including credit cards, personal bank loans, payday loans, tax debt, and student loans if at least seven years have passed since you were last a student.

When a Consumer Proposal Is the Stronger Choice

A consumer proposal tends to serve you better if you have a steady income and assets you want to protect. "When a person wants to keep their assets, they usually file a proposal rather than a bankruptcy. In a proposal, your assets are off-limits," points out Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.

The monthly payment math also favours proposals for many debtors, even though the total repayment amount is higher than what bankruptcy would cost. Kroll explains how this works in practice: "Let's assume you have an unsecured debt of $50,000. And let's assume in a bankruptcy the debtor would have to pay $5,000 on $50,000. Creditors are unlikely to accept much less than $20,000. However, maybe they'll take $15,000. With a proposal, you could pay $15,000 over five years as opposed to $5,000 over 9 months or 21 months. So the amount of money per month that you have to pay is better with the proposal than with the bankruptcy. And it also means you didn't have to file for bankruptcy," explains Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.

Consumer proposals also carry fewer ongoing duties. Once your monthly payment is set, it does not change, regardless of whether your income rises or falls. In bankruptcy, increased earnings can trigger higher surplus income payments and extend the timeline. You also avoid monthly income and expense reporting that bankruptcy requires.

The credit rating implications matter beyond just the score. Jeff Schwartz, Executive Director of Consolidated Credit, puts it bluntly: "Bankruptcy has a much more dire impact when a lender is looking at your profile going forward. Also, it's not for somebody who depends on their credit for their job. If they're in financial management or they're working for a bank or an insurance company, many of these organizations are going to look at their credit report and make a decision," explains Jeff Schwartz, Executive Director of Consolidated Credit.

If your profession is regulated or your employer conducts credit checks, the difference between an R7 notation and an R9 bankruptcy notation can directly affect your livelihood.

When Bankruptcy Makes More Sense

Bankruptcy is not always the worse option. If your income is low or unstable, creditors may not accept a consumer proposal because you cannot demonstrate the ability to make consistent payments over several years. If you have lost your job and have no realistic prospect of funding a proposal, bankruptcy may be the only path to relief.

Bankruptcy also has no upper debt limit. If you owe more than $250,000 in unsecured, non-mortgage debt, you cannot file a standard consumer proposal and bankruptcy becomes the primary route. The process also concludes much faster. A first bankruptcy with no surplus income can end in nine months assuming you have no surplus income or 21 months otherwise, which means you could begin credit rebuilding years before a five-year consumer proposal would finish.

It is a common misconception that bankruptcy leaves you with nothing. Every province maintains a list of exempt assets that creditors cannot seize. These typically include basic household furnishings, clothing, food, a vehicle up to a specified value, medical aids, and tools required for your trade. The specifics and dollar thresholds vary by province, so you should verify your provincial exemptions with your LIT.

How To Decide

The decision between a consumer proposal and bankruptcy requires a detailed assessment of your income, assets, total debt, and personal circumstances. No online comparison chart can replace a consultation with a Licensed Insolvency Trustee, which is offered at no cost. During that meeting, the LIT will calculate what you would pay under each scenario, identify which assets are at risk in a bankruptcy, and determine whether your creditors are likely to accept a proposal.

Start by listing your total unsecured debts, your monthly household income, and the current value of your major assets. If your unsecured debt is under $250,000, you have income to support monthly payments, and you own a home or other assets you want to retain, a consumer proposal will almost certainly be the better fit. If your income is minimal, you have few assets, and you need the fastest possible resolution, bankruptcy deserves serious consideration.

Related Posts

View All

10 Unexpected Effects of Doing a Consumer Proposal in Canada

Unlike bankruptcy, a consumer proposal does not transfer control of your assets to a trustee. You keep your home, your vehicle, and all your investment accounts.

10 Surprising Items You Can Legally Keep Thanks to Canadian Bankruptcy Exemptions

Arguably the biggest misconception about Canadian bankruptcy is that you will automatically lose your car.

The Pros & Cons Of Declaring Bankruptcy in Canada

“I think filing for bankruptcy can prevent heart attacks, suicide, divorce, and job loss because people can now focus on life, as opposed to fighting with creditors they cannot afford to pay,” argues Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.