Updated on July 2, 2026 · Published on April 15, 2026 · 4 min read

If you are searching for the best no-fee bank account in Canada, these four options charge zero monthly fees while still offering competitive interest, unlimited transactions, and modern digital tools. Here is what each one delivers and where they differ.

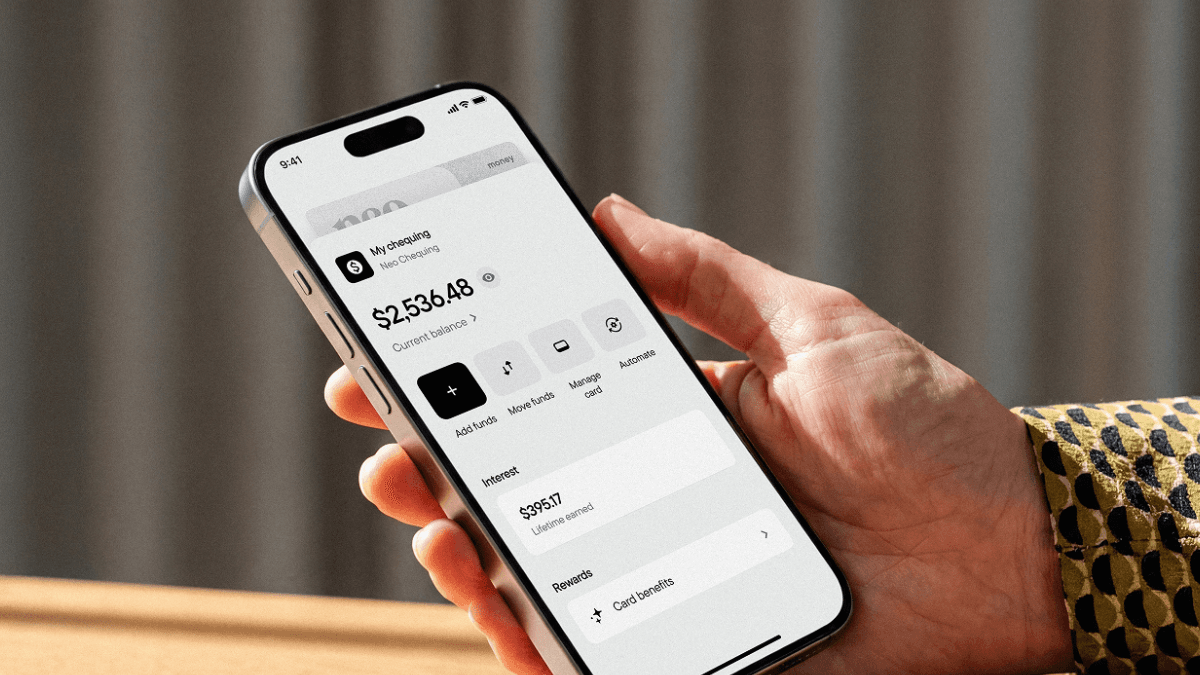

1. Neo Chequing Account

In a Neo Chequing account, your deposits earn 0.1% on everyday chequing balances on every dollar, and you can make unlimited transactions without extra charges. The account pairs with a Neo Money card, a prepaid Mastercard that earns cashback: 1% on gas and groceries and up to 5% at thousands of partner retailers across Canada. Funds are held at a member institution of the Canada Deposit Insurance Corporation (CDIC), so deposits receive the same federal protection you would get at a traditional bank. You manage everything through the Neo app, and e-Transfers are free to send and receive. Another advantage of banking with Neo is that we do not charge NSF fees. For those seeking a higher interest rate, the Neo Savings account offers a generous interest rate of up to 3% and funds can be transferred between Neo accounts instantly.

2. EQ Bank Personal Account

EQ Bank's Personal Account has become one of the most popular no-fee options in the country. It charges no monthly fees, requires no minimum balance, and offers unlimited free transactions including Interac e-Transfers. EQ Bank consistently provides one of the higher everyday interest rates among Canadian digital banks (a 1.00% base rate that jumps to 2.75% when you set up qualifying direct deposits), which means your chequing balance actually grows. The bank also provides free international money transfers through Wise integration, joint account options, and CDIC deposit insurance. One limitation is that EQ Bank does not have a physical branch network or traditional ATM access without its card, though its prepaid Mastercard now offers free withdrawals at any Canadian ATM by reimbursing the fees. Additionally, the bank does not charge NSF or overdraft fees, so you need to be comfortable with fully digital banking.

3. Simplii Financial No Fee Chequing Account

Simplii Financial, a division of CIBC, offers a No Fee Chequing Account that includes unlimited debit purchases, bill payments, and withdrawals at zero cost. You also get free access to more than 3,400 CIBC ATMs across Canada, which is a significant advantage if you regularly need physical cash. Simplii provides a Debit Mastercard for online and in-store purchases wherever Mastercard is accepted. Overdraft protection is available for a $4.97 monthly charge (only when used) plus 19% annual interest on overdraft balances, while accounts without this protection are subject to a $10 NSF fee. The account pays a small amount of interest on deposits (tiered between 0.01% and 0.05%), though rates are lower than what you will find at Neo or EQ Bank.

4. Tangerine No Fee Chequing Account

Tangerine, a subsidiary of Scotiabank, offers a chequing account with no monthly fees, no minimum balance requirement, and unlimited free debit transactions. You get free access to Scotiabank's ATM network across Canada, which numbers roughly 3,500 machines. Tangerine provides a Visa Debit card, free Interac e-Transfers, and mobile cheque deposit. The bank occasionally runs promotional interest rates on new chequing accounts, but the standard everyday interest rate on chequing balances sits lower than dedicated high-interest accounts (tiered between 0.01% and 0.10%). Optional overdraft protection is available for a $5 fee per use plus 19% annual interest; without it, a $10 NSF fee applies. Tangerine also offers automatic savings features that round up purchases or move money on a schedule, which can help with budgeting.

How No-Fee Banks Actually Make Money

A common question is how these institutions survive without monthly fees. Like traditional banks, online banks make money by acting as middlemen. When you put your cash into a "free" account, the bank uses that money to fund loans like mortgages and lines of credit. They pay you a tiny bit of interest for the use of your money, but they charge borrowers a much higher rate. They also get a cut every time you buy something. When you tap your card at a grocery store or a shop, the merchant pays a small percentage of that sale back to your bank. This is what the banking industry calls the interchange fee.

Tim Morris, Chief Banking Officer at Neo Financial, explains that online banks are just more capital efficient than traditional banks: "The way that traditional banks make money is similar to the way that virtual challengers do. One key difference is that traditional banks have more overhead in terms of manual processes and a physical network of branches. Virtual banks will often use this advantage to deliver more benefit to customers across their financial products”, observed Tim Morris, Chief Banking Officer at Neo Financial.

By Julien Brault

Julien Brault is a fintech entrepreneur and personal finance expert dedicated to making financial literacy accessible to all Canadians. As the founder of MooseMoney, he currently focuses on helping individuals navigate financial struggles through actionable advice and financial calculators.

Related Posts

View All

Should you open a joint chequing account? Here’s what you need to know

Learn how a joint chequing account works in Canada, who can open one, and how the joint Neo Chequing account makes shared spending simpler.

The complete guide to joint accounts in Canada

What is a joint bank account? Learn how joint accounts work in Canada, who can open one, the pros and cons, and how to pick the right account.

These credit cards earn the most cashback on gas in Canada

Compare the best gas credit cards in Canada by cashback rate, annual fee, and perks. See which card gives you the highest return at the pump in 2026.