Published on July 2, 2026 · 4 min read

By Julien Brault, founder of MooseMoney.

Before opting for bankruptcy, Canadians should make sure they understand the pros and cons of such a move. They should also compare it to other debt relief options like a consumer proposal.

From our sponsor

The Pros of Declaring Bankruptcy

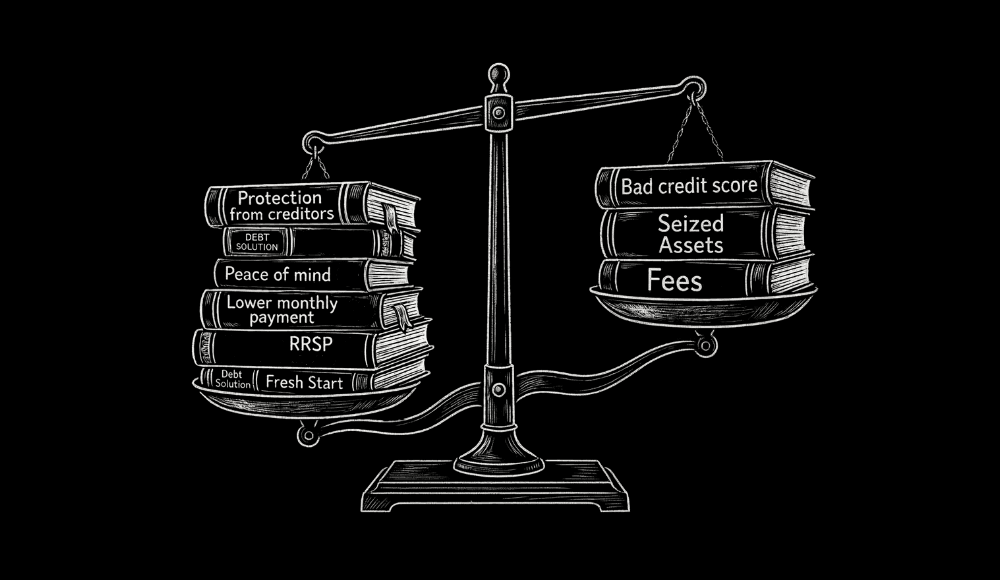

The most immediate benefit of filing for bankruptcy is the stay of proceedings, which provides instant legal protection by stopping your creditors from contacting you. “I think filing for bankruptcy can prevent heart attacks, suicide, divorce, and job loss because people can now focus on life, as opposed to fighting with creditors they cannot afford to pay,” argues Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.

Bankruptcy also eliminates most of your unsecured debts, including credit card balances, lines of credit, payday loans and even personal income tax debt. For a first-time bankruptcy, this process can often be completed in just nine months, assuming your are not earning enough to be considered having "surplus income".

You also do not lose all your possessions since you are allowed to keep essential assets. This usually includes household furniture, clothing, tools needed for work, and a vehicle up to a certain value, along with most registered retirement savings plans.

The Cons of Declaring Bankruptcy

Filing for bankruptcy still comes with a financial cost, primarily the fees paid to a Licensed Insolvency Trustee to administer the process. If your household income is above a specific standard set by the government, you will be required to make surplus income payments. Earning above this threshold means your monthly payments increase, and your bankruptcy could be extended from nine months to 21 months.

You will also lose your non-exempt assets because a trustee will liquidate them to repay your creditors. This includes any equity in your home, tax refunds and unexpected windfalls like inheritances or lottery winnings.

Furthermore, bankruptcy does not clear all debts. Secured debts backed by collateral, such as mortgages and auto loans, are not discharged. You also remain responsible for child support, spousal support, court-ordered fines, and student loans that are less than seven years old.

If you have joint loans, bankruptcy will negatively affect your co-signer because the full responsibility for the debt will transfer entirely to them. If they cannot pay, their credit rating will suffer.

Finally, bankruptcy creates specific occupation barriers. Many employers mandate credit score and criminal record checks for executive positions. If you are an accountant, you could even lose your Chartered Professional Accountant license. You are also legally forbidden from being a director of a company while you are bankrupt.

The Pros and Cons of Bankruptcy for Your Credit File

Filing for bankruptcy directly alters your credit history and changes how lenders view your financial profile. It is crucial to understand exactly how this legal step affects your ability to borrow money and rebuild your credit over time.

The Pros

While the negative impacts are significant, they are temporary. This drop in your credit score might not be a major issue if your credit is already poor from unpaid bills and collections.

Going bankrupt does not make it impossible to get credit, as there are various ways to access credit even while you go through the process. You can apply for tools like the Secured Neo Mastercard to safely establish a new payment history. The required counselling sessions also give you the skills to rebuild your credit and improve your financial health after your discharge.

“People who do not go back into debt learn to use credit properly. They learn from their mistake of overspending. They provide for a rainy day fund so that they don't get caught by having to dive into debt again if something happens,” observes Jeremy Kroll, Licensed Insolvency Trustee and Partner at Baigel Corp.

The Cons

The most obvious drawback is the severe impact on your credit rating, as you will receive an R9 rating, which is the lowest possible score.

“Bankruptcy is going to remain on your public record forever. It's going to remain on your credit report for seven years for the first one and then 10 years for the second one” says Jeff Schwartz, Executive Director of Consolidated Credit.

A record of bankruptcy will remain on your report for six to seven years following your discharge, and you will lose all your credit cards. It may be difficult to borrow money during this period and any loans you do get approved for will likely come with much higher interest rates and less favorable terms.

Related Posts

View All

Bad credit car loans in Canada: How to get approved

Bad credit car loans are available in Canada, but the terms vary widely. Here’s how to find one that won’t cost you more than the car itself.

Joint account tax implications in Canada: Who pays what to the CRA?

Interest, dividends, and capital gains earned in a joint account are all taxable, but they aren’t necessarily split 50/50. Here’s what the CRA actually expects you to report.

How to keep your house through a consumer proposal in Canada

If your home equity in lower than the bankruptcy exemption in your province (less than $10,783 in Ontario, for example), your proposal can be lower than the amount you owe, even if you own house.