Published on March 30, 2026 · 4 min read

By Julien Brault, founder of MooseMoney.

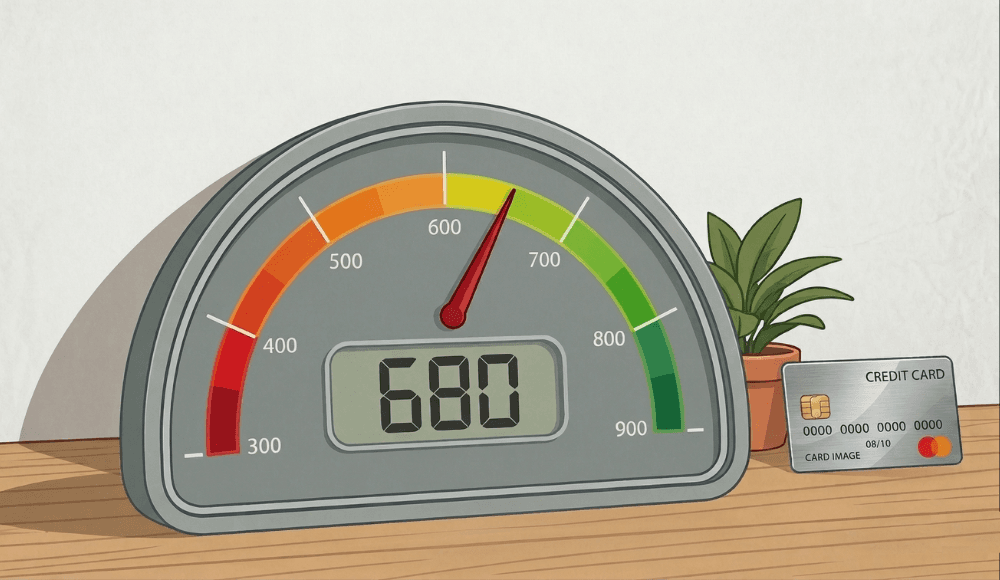

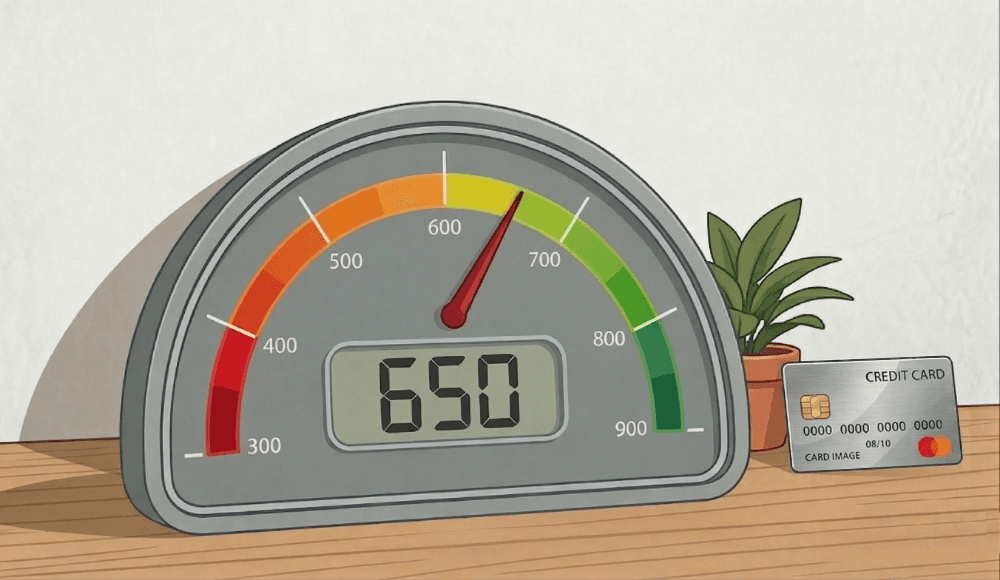

A 680 credit score in Canada falls within the "good" range, as Equifax categorizes scores between 670 and 739 as good. It also sits above the average Canadian credit score of 650, according to TransUnion data. That means most standard credit products are within reach, but you will likely face limitations on premium products and competitive interest rates.

"A 680 credit score would be a reasonable credit score to get most products. You'd probably get in the wheelhouse for a lot of credit cards, personal loans and auto finance. Things like a line of credit, you'd probably get if it's secured or if it's a small line of credit," stated Matt Fabian, Director of Financial Services Research at TransUnion.

In practical terms, a 680 score should qualify you for most no-fee and mid-tier credit cards, including cashback options like the Neo Mastercard, which does not require a top-tier score for approval. You can expect approval for most personal loans and auto financing as well, though the interest rates you receive will reflect the moderate risk lenders associate with this score band. Secured lines of credit and smaller unsecured lines of credit are also realistic, but larger unsecured credit lines with favourable terms may be harder to access.

Mortgages are where things get more complicated. Most lenders require a minimum credit score of 680 for a conventional mortgage, which means you are right at the threshold. Matt Fabian from TransUnion put it plainly: "Mortgages will be a bit tighter at 680. I'm not saying you couldn't get it. But you might not get the best rate for that mortgage because they're pricing the risk." Even a small difference in your mortgage rate can cost you thousands of dollars over the life of the loan, so improving your score before applying could save you real money.

Premium travel rewards credit cards, top-tier cash back cards with high earn rates, and large unsecured lines of credit at prime or near-prime rates are generally reserved for borrowers with scores of 740 and above. You will also have less negotiating power on interest rates for any loan product compared to someone in the "very good" or "excellent" range.

What You Can Realistically Access at 680

You can qualify for most standard credit cards, including no-annual-fee cashback cards and some mid-tier rewards cards. Auto loans and personal loans are accessible, though expect rates above what lenders advertise to their best-qualified borrowers. Secured lines of credit and small unsecured lines of credit are attainable. Rental applications should go smoothly, since most landlords who run credit checks consider 680 an acceptable score. You also meet the minimum threshold that most conventional mortgage lenders set, even if you will not get their best advertised rate.

What Will Be Harder or More Expensive

You will pay more in interest on almost every product compared to someone with a score above 740. Premium credit cards with large sign-up bonuses and comprehensive travel insurance packages typically require higher scores. Unsecured lines of credit with competitive rates and higher limits will be difficult to obtain. Your mortgage options will be narrower, and you should expect to be quoted rates above the lowest advertised offers. Some lenders may also require a larger down payment or additional documentation to offset the perceived risk.

How to Move Your Score Higher

The fastest way to improve a 680 score is to lower your credit utilization ratio by paying down existing balances. Aim to keep utilization below 30% of your total available credit. Make every payment on time, since payment history is the single largest factor in your score calculation. Avoid applying for multiple new credit accounts in a short period, because each hard inquiry can temporarily reduce your score. Keep your oldest credit accounts open, even if you rarely use them, since the length of your credit history contributes positively. Check your credit reports through Equifax and TransUnion at least once a year to catch errors, and dispute any inaccuracies immediately.

A 680 credit score gives you access to most of what you need in Canada's credit market, but it costs you money on nearly every product through higher interest rates. Moving your score into the mid-700s is where the real savings begin, and for most people, that jump is achievable within six to twelve months of disciplined credit management.

Related Posts

View All

Does Getting Your Rent Payments Reported to Credit Bureaus Actually Help You Build Your Credit in Canada?

Over the last few years, various rent reporting services have emerged in Canada, most of which only report rent payments data to Equifax. That includes Borrowell Rent Advantage, FrontLobby, and KOHO. More recently, rent reporting company Zenbase anno

What You Can and Can't Do With a 650 Credit Score in Canada

You can still qualify for car loans, high interest personal loans, and secured credit cards, but you will face higher interest rates.

How to Freeze Your Credit and Avoid Credit Fraud in Canada

"If you're concerned about people opening up credit in your name or if your info were part of a leak, freezing your credit file is something you should consider."