5 reasons why Canadian virtual banks are gaining ground over Canada's big banks

Updated on June 30, 2026 · Published on April 15, 2026 · 3 min read

Virtual banks in Canada are pulling customers away from RBC, TD, BMO, Scotiabank, and CIBC by offering higher savings rates, lower fees, and faster account setup. According to the Canadian Banking Association, 77% of Canadians do most of their banking virtually. That shift is accelerating as digital-only players like Neo Financial deliver tangible financial advantages that the Big 5 have been slow to match. Here are the five specific reasons driving the change.

1. Branches Matter Less Than They Used To

Tim Morris of Neo Financial framed this shift clearly: "There are millions of Canadians who are getting a better experience out of virtual banks than they are from the traditional experience of having to physically go to a branch in person." The data supports him. The average number of monthly branch visits per Canadian dropped from 1.8 in 2021 to 1.3 in 2024, and only 12% of customers now do most of their banking at a branch. The number of physical bank branches in Canada has been declining since 2014, falling from 5,890 in 2018 to around 5,656 by 2022.For the growing majority of Canadians who handle every transaction digitally, the branch is no longer a reason to stay, and the fees that fund it are increasingly a reason to leave.

From our sponsor

-QkWZHU1Pc7iPOpNuO2OoiY1XJnD8W7.png&w=1920&q=75)

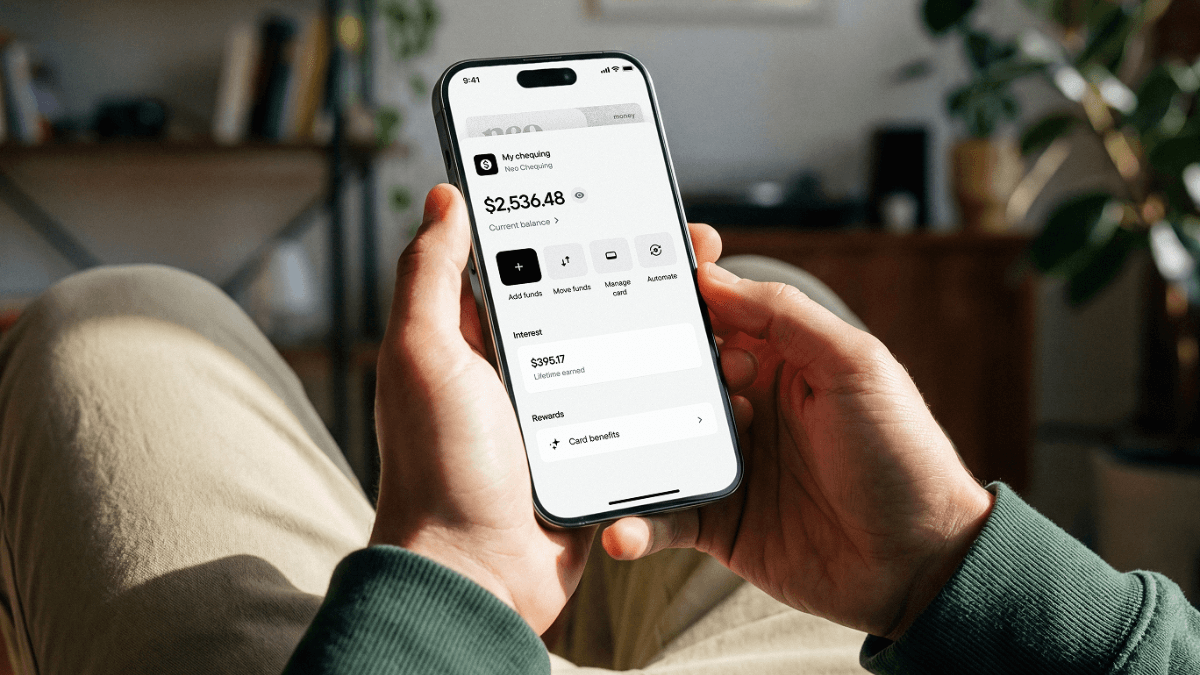

2. Big Bank's Savings Interest Rates Are Laughable

Traditional Big Banks’ savings accounts typically pay between 0.01% and 0.05% on deposits, which is functionally zero. Virtual banks offer substantially more. The Neo Savings Account currently pays 3% with no monthly fees. For a Canadian holding $25,000 in savings, the difference between 0.05% at a Big 5 bank and 3% at Neo translates to roughly $747.90 more in annual interest.

3. Big Bank's Monthly Fees Have Become a Dealbreaker

The Big 5 banks charge monthly chequing account fees that typically range from $4.95 to $32.95 unless customers maintain minimum balances of $3,000 to $6,000. Most virtual banks in Canada have eliminated monthly fees entirely. Neo Financial's chequing account costs $0 per month with no minimum balance requirement. Over a year, a Canadian paying $16.95 per month at a traditional bank spends $203.40 just to hold a chequing account. Virtual banks avoid this cost because they do not operate physical branches, employ tellers, or maintain the overhead that brick-and-mortar locations demand.

4. Canadians Are Fed Up With Big Banks' Gotcha Fees

Monthly fees are only the most visible part of the problem. The Big 5 have built entire revenue streams on various charges. NSF fees are the starkest example. Before the government capped NSF fee at $10, Big 5 banks charged as much as $48 per NSF incident, generating around $753 million in annual fee revenue for banks. Big banks also routinely charge their customers up to $1 for sending Interac e-transfers, up to $2 for using their own ATM and so on. The Neo Everyday Account, on the other hand, carries no monthly fees, never charges any NSF fee, and allows its users to send up to 50 Interac e-transfers per month free of charge.

5. Canadians Are Looking For A Mobile-First Experience

The Big 5 banks did not design their digital platforms from scratch. They layered apps on top of core banking systems that were built decades ago, and the experience often shows. Meanwhile, mobile banking usage among Canadian account holders grew from 53% in 2019 to over 60% by 2025. Neo Financial was designed from the ground up as a mobile product. Opening an account takes minutes and requires nothing more than a phone, a government ID, and a selfie. There is no branch visit, no paper form, and no waiting period before a virtual card is available to use.

By Julien Brault

Julien Brault is a fintech entrepreneur and personal finance expert dedicated to making financial literacy accessible to all Canadians. As the founder of MooseMoney, he currently focuses on helping individuals navigate financial struggles through actionable advice and financial calculators.

Related Posts

View All

Should you open a joint chequing account? Here’s what you need to know

Learn how a joint chequing account works in Canada, who can open one, and how the joint Neo Chequing account makes shared spending simpler.

The complete guide to joint accounts in Canada

What is a joint bank account? Learn how joint accounts work in Canada, who can open one, the pros and cons, and how to pick the right account.

These credit cards earn the most cashback on gas in Canada

Compare the best gas credit cards in Canada by cashback rate, annual fee, and perks. See which card gives you the highest return at the pump in 2026.